Archive for the ‘Uncategorised’ Category

Liberalising capital controls on Icelanders – who don’t really notice

The Ministry of finance has now introduced the third and last significant step towards lifting capital controls. After lifting controls on the estates of the failed banks last year and the disputed action earlier this year to solve, or box in, offshore króna holders, it’s now as promised since the elections in 2013 time to lift controls on Icelanders, both individuals and companies, just in time for the coming election on October 29. All but the very wealthiest Icelanders will now be outside controls. And Icelanders? They don’t pay much attention to this latest step.

Ordinary Icelanders have not much felt the capital controls in their daily lives since the capital controls only cover investment but now those wealthy enough to want to buy property abroad or invest in foreign companies etc. can do so. The main points are the following, according to the Ministry of finance press release:

- That outward foreign direct investment be unrestricted but subject to confirmation by the Central Bank of Iceland.

- That investment in financial instruments issued in foreign currency, other monetary claims in foreign currency, and prepayment and full payment (retirement) of foreign-denominated loans be permissible up to a given amount, upon satisfaction of specified conditions.

- That individuals be authorised to purchase one piece of real estate abroad per calendar year, irrespective of the purchase price and the reason for the purchase.

- That requirements that residents repatriate foreign currency be eased and that they be lifted entirely in connection with loans taken abroad by individuals for real estate or motor vehicle purchases abroad, or for investment abroad.

- That various special restrictions be eased or lifted entirely, including individuals’ authorisation to purchase foreign currency for travel.

- That the Central Bank of Iceland’s authorisations to gather information be expanded so that the Bank can promote price stability and financial stability more effectively.

As of 1 January 2017, the following are to take effect:

- The ceiling on investment in financial instruments issued in foreign currency, other monetary claims in foreign currency, and prepayment and full payment (retirement) of foreign-denominated loans will be raised.

- Transfers of deposit balances will be permissible for amounts below a certain ceiling. The requirement for domestic custody of foreign securities investments will be revoked. This will enable residents and non-residents to transfer deposits and securities to and from Iceland and to trade in securities abroad within the limits specified in the bill.

- Individuals’ authorisation to purchase foreign currency in cash will be expanded significantly.

Capital controls lifted in a record boom

All of this is made easier since Iceland is enjoying a record boom with tourism flourishing and more foreign reserves compared to more or less any time in the country’s recent history. As I’ve mentioned earlier, Icelandic authorities don’t regard it as a problem that the largest offshore króna holders are preparing to test in court(s) the earlier decisions regarding the offshore króna, i.e. either a haircut in an auction or a lock-in with 0.5% interest rates, effectively negative in Icelandic context and no expiry date. Nor does the comparison with Argentina seem to cause worries in Iceland.

Easing out of the capital controls is obviously a hugely important step for Iceland. Yet, it has mostly gone unnoticed in the media. The reason is that people normally haven’t noticed the controls except in minor things like having to bring a flight ticket in order to buy travel currency. For those running companies it’s been a different story, the controls have both been annoying and harmful. Measuring losses due to capital controls isn’t easy but in 2014 The Icelandic Chamber of Commerce estimated it to be ISK80bn annually. As the CBI and others have frequently pointed out the longer controls remain in place the greater the harm.

The CBI has put in place safety measures re foreign inflows. Some claim this means that controls are still in place but that’s certainly not how I see it. By 2012 the CBI had already announced in a report, Prudential Rules Following Capital Controls, that as well as lifting capital controls the bank would also develop financial stability rules in order to temper foreign inflows if needed, much like other countries with have done such as Asian countries under similar circumstances.

Collapse measures out, political distrust in

Alors, after almost eight years with capital controls Iceland has now almost entirely graduated from that part of the banking collapse, certainly a significant step towards normality. The question is still if the second measure, i.e. re offshore króna holders, will come back to haunt the country.

Though the emergency measures from 2008 have disappeared over the years politically the collapse still looms large in Icelandic politics. It’s not that the collapse itself is frequently discussed, not at all, but it shapes the hues and colours of the political debate. Quite specifically, the collapse has inter alia stoked distrust in politicians both in general and in certain politicians, due to their stories, still looms large. Icelanders are willing to throw their trust on new parties, next to be tested in the coming election.

One obviously prudent measure not introduced in Iceland is the separation of retail and investment banking. Three governments have ignored doing this, meaning that there is probably a silent political will to sell Landsbanki and Íslandsbanki without this safety measure. Hugely indicative of the influence of powerful private interests, quite worrying for the public interest.

Now, mostly free of restraining controls the Icelandic króna, the currency of the world’s smallest independent economy with own currency, will again be free (with the safety jacket of financial stability rules) to float in the large ocean of international finance. Trying times await booming Iceland, testing if the right lessons were learnt in 2008.

*Here is an earlier blog on the offshore króna problem and potential litigation; here is the latest one on offshore króna holders and their US political contacts.

Fitch has downgraded “Iceland’s Long-Term Local Currency (LTLC) IDR to ‘BBB+’ from ‘A-‘. The Outlook is Stable.” – The downgrade results not from Icelandic conditions but are due to changes Fitch has introduced to reflect regulatory changes, see here.

Follow me on Twitter for running updates.

Old and new powers in Greece – and the ELSTAT case

The re-awoken charges against ex-ELSTAT head Andreas Georgiou and two of his colleagues are attracting attention in the international media. Last, the Financial Times takes the case up on its front page today. According to recent report on EurActiv it also seems that powers in Brussel are rightly getting increasingly worried about the procedures in Greece against Georgiou.

After a trip to Athens last year I wrote about the case in detail on Icelog. When the case resurfaced now in summer I pointed out that Greek authorities were punishing the messenger instead of those who really falsified Greek statistics for roughly a decade.

The reason I find the ELSTAT case so interesting and important is that in my view it’s a test case for the willingness of the Greek political class to face the misdeeds of the past, the corruption and all the things that hinder prosperity in Greece. In addition, a country without reliable statistics can’t really claim to be a modern and accountable country.

As it is now, Greece is heading towards a political trial where those who fixed the fraud are being hounded and punished, not the perpetrators. As long as the charges against Georgiou and his colleagues are upheld it is clear that the forces who want to keep Greece as it was – weakened by corruption and unhealthy politics – are still ruling. That isn’t only worrying for Greece but for Europe as a whole.

Follow me on Twitter for running updates.

Offshore króna holders with interesting friends

Holders of Icelandic offshore króna holders seem to have gained some intriguing friends. A so-called think tank, Institute for Liberty with the slogan “Defending America’s Right To Be Free” has suddenly found the urge to set up a project called “Iceland Watch” with its own website, specifically to follow, it seems, how Icelandic authorities deal with offshore króna holders (inter alia linking to some of my blogs).

The focus of interest, according to the Institute, is the following:

“The Institute for Liberty has followed Iceland’s path to recovery since the 2008 collapse and has developed an increased concern over recent protectionist economic policies like the discriminatory practices against offshore króna investors.

“In creating Iceland Watch, we aim to keep the public apprised of any anti-democratic and anti-free trade policies put into place by the Althingi, Iceland’s parliament, which could threaten the property rights of offshore investors in Iceland’s króna.

“Holders of Iceland’s offshore krona include several American investors, which serve a variety of retail investors like retirees with 401k plans and institutional investors such as corporate and public retirement plans, foundations, and endowments.

“Despite investors’ willingness to support Iceland during its time of transition and several distinct offers to negotiate good faith solutions, the Icelandic government refuses to offer anything other than a clear take-it-or-leave-it scenario. The discrimination against foreign investors is disturbing and could affect millions of American holders of 401k and retirement accounts.

“When Iceland’s parliament, the Althingi, convenes its Summer Special Session on August 15, its actions will indicate whether the island nation will reintegrate itself into international free markets or further its isolation by instating new costly, misguided policies that chill investment and economic growth.”

The Institute’s website indicates it’s also interested in Puerto Rico’s debt, another place where American investment funds struggle to get repaid. More intriguingly, the Institute has also fought Obamacare and other typically far-right interests.

Indeed, the Institute is part of ad hoc networks of “think tanks,” non-profit organisations and ,,grassroots” organisations funded by far-right American billionaires such as David and Charles Koch and the hedge fund owner Paul Singer, who for years fought the Argentinian government, now a settled issue.

The Institute is mentioned in Jane Mayer’s insightful and well-documented analysis of the money powers on the right-wing of the Republican party, far more right-wing than the mainstream Grand Old Party is. Powers, that for a few decades have pumped money into setting up phoney “grassroots” organisations in support of the tobacco industry, against environmental issues and lately, Obamacare. Mayer’s book, Dark Money; The Hidden History of the Billionaires Behind the Rise of the Radical Right, came out in spring, an essential read to understand the undercurrents in US politics the last decades and the issues behind political funding, now open to anonymous donations, and the Citizens United ruling in 2010.

According to Mayer, Institute for Liberty got lucky with funding, yet another node in the efforts to fight Obamacare; in 2009 it received $1.5m:

Four hundred thousand dollars of these funds were channeled back to DCI Group (Washington PR company, instrumental according to Mayer in fighting Obamacare) for “consulting.” The previous year, the Institute for Liberty’s entire budget had been $52,000. Suddenly it was so awash with cash that the group’s president, Andrew Langer, told the The Washington Post,‘ “This year has been really serendipitous for us.” He said a donor, whom he declined to name, had earmarked the funds for a five-state advertising blitz targeting Obama’s health-care plan. (Mayer, p.192).

As I’ve pointed out earlier, there have been some articles popping up here and there – op-ed in WSJ, guest blog on FT Alphaville and the most recent on The Street, “Iceland Should Learn From Argentina’s Bad Example” by Aldo Abraham, an Argentinian academic.

No need to point out that of course all of the media rumbling is orchestrated, driven as it is by non-journalistic input; as seen from Mayer’s book the DCI Group has links to the Institute. Everyone fights their turf as best they can, the links to the knights of dark money is rather unsettling but “à chacun son goût.” It is intriguing to see the cause of Icelandic offshore króna holders as part of this picture: not necessarily surprising but yes, intriguing.

The Princeton economist Angus Deaton, summarises masterly in his powerfully argued “The Great Escape” that the worrying trend in US politics is the tendency of interest groups to buy influence in Washington.

As spelled out in earlier blogs Argentina is potentially a worrying example for Iceland: it fought creditors and then settled after a decade of costly legal wrangling, beneficial for the lawyers involved and corrupt powers but deeply deeply harmful for Argentina. In Iceland, voices similar to those Argentinian politicians who fought the Argentinian debtors can be heard. Elections are coming up in October, politicians will hardly strife to be on the side of foreign creditors although successful plan last year re the estates of the failed banks, based on agreement with creditors, is a positive argument for co-operation with creditors.

Views vary: some claim Iceland’s cause is wholly different from Argentina. However, although Iceland has graduated from the earlier IMF program the Fund is still closely connected to Iceland; it’s difficult to imagine that the Fund’s views will be ignored. Happily, Iceland is blossoming and, according to the latest IMF report, has more than gained what it lost on the crisis, i.e. it’s difficult to argue for any emergency actions. In the end, Iceland will have to decide on the best course to follow so as to adhere to the rule of law and further prosperity.

Follow me on Twitter for running updates.

Greek authorities punish the messenger, not the culprits of fraud

In Greece, authorities go after those who tried to sort out the mess of the Greek economy, not those who created it. That’s one conclusion to be drawn for charges, yet again, brought against Andreas Georgiou former head of ELSTAT, the Greek statistics bureau. It should be scary for Greeks and European institutions to see the relentless persecutions of a civil servant who did his job.

Since he was appointed head of ELSTAT in summer of 2010, well after it was clear that the Greek statistics were unreliable, Andreas Georgiou has had to fight forces in Greece who simply refuse to let go of him and his colleagues, a story carefully recounted on Icelog a year ago, with the precise data of statistics and the development of the ELSTAT saga. Time and again, the case against Georgiou has been dropped but always brought up again.

New criminal charges now against Georgiou do not only threaten him with a prison sentence but also threaten to awaken earlier dropped charges against him and two of his colleagues.

And those who for years falsified statistics? No, not one hair on their head has been ruffled, no investigations set up as to how it was possible that wrong and falsified statistics were reported to Greeks themselves and to international bodies such as Eurostat, the European statistical bureau, more or less from 2000 until 2009.

In Game Over, the Inside Story of the Greek Crisis, George Papaconstantinou minister of finance during the fateful time from the October 2009 election until June 2011 recounts thoroughly how the falsified statistics came up as soon as the PASOK government came to power.

Already during his first days in Office, Papaconstantinou heard from various institutions that inter alia the much watched budget deficit was well beyond what the Greek authorities had reported to Eurostat two days before the October 2009 election. “In short, they had lied,” Papaconstantinou concludes in his book. What ensued was a discovery of fraudulent statistics going back years.

No one could precisely show Papaconstantinou how the reported figure was found. One of his first acts in office was to call the head of the national statistics, professor Emmanouil Kontopyrakis to his office. The professor had no idea how the deficit figure was computed but to him it did seem like a “reasonable projection” – the minister asked him to resign.

As Papaconstantinou carefully recounts much of the mistrust of his European colleagues directed at Greece was based on the fact that there wasn’t even precise statistics and figures to work with to begin with.

When Andreas Georgiou took over as head of ELSTAT in August the much-debated deficit figures, both forecasted and the real figures, had been corrected, of course greatly increasing the deficit, under the auspice of Eurostat.

As carefully detailed in my ELSTAT saga last year, the numbers kept going upwards. The 2009 deficit first forecasted 3.7% in early October was by April 2010 estimated by Eurostat to be an actual deficit of 13.6% but Eurostat was still not sure it couldn’t rise; by late 2010 Georgiou and his team found it to be 15.4%.

In his book, Papaconstantinou writes that Georgiou proved to be the right man for the job, “helping to make Greek statistics credible. I was less lucky with of the other people appointed to the ELSTAT board.” In a police investigation one board member was later discovered to have hacked Georgiou’s email account. Another member accused Georgiou of inflating the deficit figure, causing the bailout, a “totally absurd” accusation according to Papaconstantinou.

The memorandum on the Greek rescue packet was finalised May 2 2010. Yet, Georgiou, who only took over in August 2010, is continuously persecuted for having influenced the bailout.

Considering how poisonous the unreliable data proved to be in the discussions up to the May 2010 memorandum it would have been greater reason to thank Georgiou and his team for delivering sound statistical data.

But that is not what happened and things didn’t stop there. The opposition lapped up the accusations. “Soon the justice system was involved. Prosecutors brought criminal charges against Georgiou for actions having caused billions of damage to Greece. We were suddenly in a parallel universe; rather than bringing to task those who had lied about the true size of the deficit, we were accused for having told the truth!”

No matter though Georgiou’s case has been thrown out several times the dark forces in Greek politics always find a way of bringing it back. And that has now happened again, the case is being brought back in a new guise (see here and here). It seems that Europe risks having a political prisoner within its boundaries, imprisoned for doing his job.

Follow me on Twitter for running updates.

Next step by offshore króna holders: call the IMF

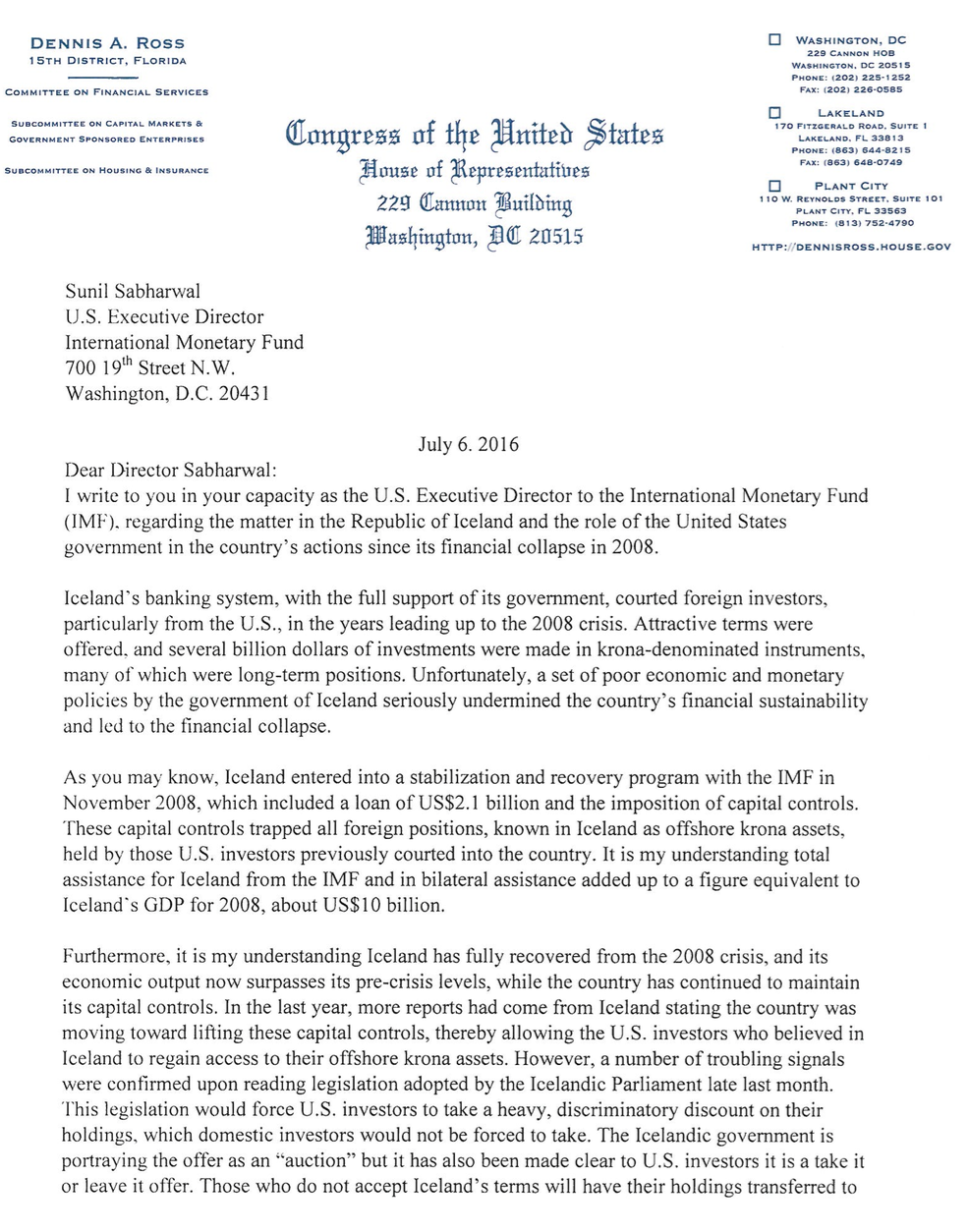

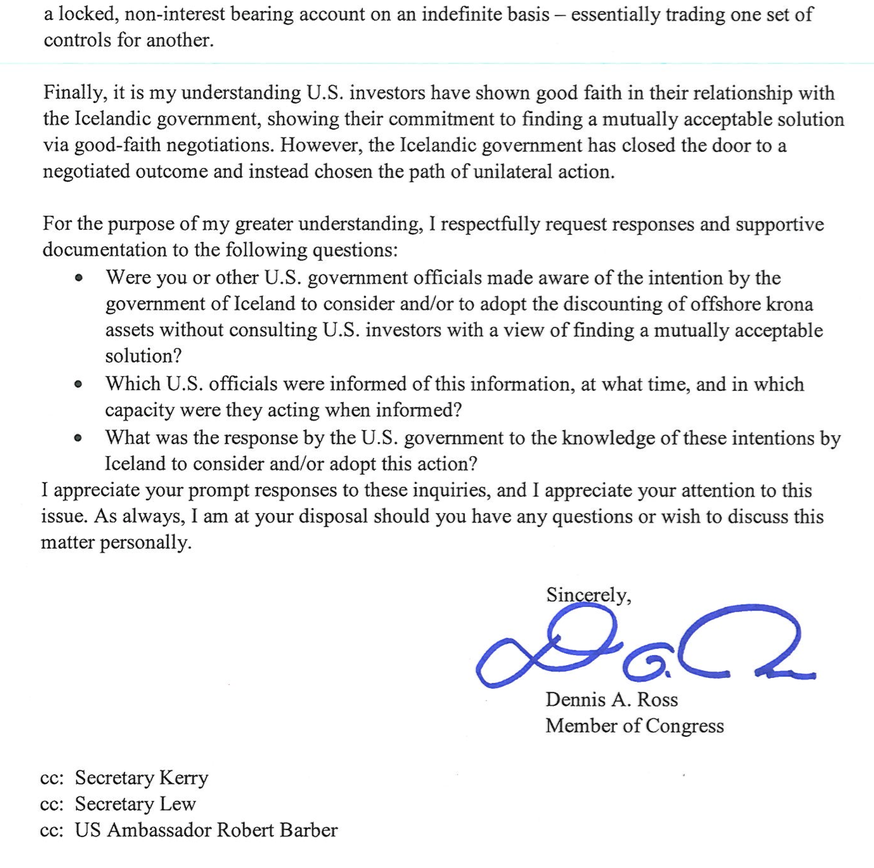

Congressman Dennis A Ross has written a letter, see below, to Sunil Sabharval, US Executive Director at the International Monetary Fund, IMF, inquiring as to what US officials knew about the offshore króna actions taken by the Icelandic government. The Congressman’s mission is clearly to safeguard US interests, i.e. the interest of US funds holding offshore króna, a problem I have dealt with extensively in earlier blogs, inter alia here. Although not stated explicitly, the most sensitive underlying assets are sovereign securities, payable in Icelandic króna.

In the letter the reasons for the Icelandic collapse are somewhat simplified to say the very least, apparently easier to blame the government than the banks; also rather funny to see the offshore króna holders treated as entirely blameless lured by good deals, another saga.

The thrust of the letter is that since Iceland has now recovered well from its 2008 crisis Iceland shouldn’t be discounting the offshore króna or offering the investors punitive terms. – Further to this: intriguingly, Iceland had not made a loss on the 2008 banking crisis but a gain of 9% of GDP(!), according to the latest IMF Article IV Consultation statement on Iceland, from June 22.

The Congressman points out that the offshore króna holders (i.e. the largest holders) have come up with various solution but Icelandic authorities have been unwilling to take any notice. He now wants to know if US officials are aware of what is going on – and he expects an answer, which as far as I know has not yet been given. IMF has preached a cooperative approach to lift capital controls, reiterated in its June statement on Iceland but seems to consent with the action taken by Icelandic authorities re the offshore króna.

Here is Congressman Ross’ letter:

Last time, this time – in general

As I recounted at length in the years, months and days up to the plan to lift capital controls on the estates of the banks, presented June 8 last year, Icelandic authorities dithered for long due to infighting until they took the plunge – to be fair, the authorities claimed it just took time to prepare the plan and refused all allegations of infighting. But the plunge wasn’t taken until it was clear the plan was supported by the largest creditors.

The same now with the offshore króna action, it all took longer than had been planned, my understanding is that it took long because of different views; however, those involved say it just took the time it took, complicated matters etc. Yet, this time the government acted unilaterally, no agreement with the largest offshore króna holders. Thus inter alia the above letter, I assume.

The government claims the offshore króna holders do not act as a group, contrary to the creditors to the old banks. That isn’t wholly correct – each estate had to be dealt with separately and support was sought for each estate. Thus, the creditors were not a unified group but three groups. So much for that argument now re the offshore króna holders.

As a ground for pride Bjarni Benediktsson minister of finance has pointed out that there was no legal aftermath to the plan last year. Quite true but that’s because the plan wasn’t passed until creditors’ support was ensured. Which is exactly the opposite of now where the government has acted unilaterally re the offshore króna holders who consequently have taken the first steps towards legal action.

In addition, there is the concern Congressman Ross shows, as well as articles in the Wall Street Journal and FT Alphaville, as I have mentioned in earlier blogs – offshore króna holders are clearly trying to point out to the world that Iceland, by planning a haircut on the offshore króna assets (when they are converted into foreign currency) doesn’t intend to honour its international commitments.

Last time, this time – in particular

I have earlier pointed out that I was wondering if the Icelandic government was going to make use of some “tricky teleological interpretation” in its dealings with offshore króna holders.

I didn’t explain in any detail what I had in mind but here it is:

Long before the June 8 plan last year, the Icelandic government claimed it couldn’t possibly have anything to do with the composition of three private banks. Right, except that composition was meaningless if it wasn’t clear beforehand how much of the Icelandic assets creditors (only 10% of the assets went to Icelandic creditors, mostly the CBI) could convert into foreign currency. Composition agreement couldn’t be reached until the government had found a solution i.e a haircut, which the creditors could agree to – that was what mostly took so long to solve.

This time, the core of the offshore króna problem is similar regarding sovereign securities. The government can claim that it’s honouring all its obligations as it will pay out any such securities in full and on time… in króna. The thing is that offshore króna holders can – or could, the auction is now over – either choose to convert at ISK190 a euro (the onshore rate is now ISK136, was ISK139 at the time of the auction) or have their króna kept on a special deposit account at 0.5% interest rates with no maturity in sight. The question is if this is seen as fair… or not.

Last year, the government came to the conclusion that it had to step in to facilitate a composition. Now, it’s just shrugging its shoulder and the message is, as I’ve stated earlier, “let them litigate” – alors, last year, the goal was to prevent legal action, this year it’s bring it on…

Follow me on Twitter for running updates.

Ukip’s sinister double bill and failed political leadership

Until early this year it seemed unlikely that an extreme idea lingering for two decades on the political fringe could turn into a mainstream choice preferred by majority of British voters as happened on June 23. Ukip’s leader Nigel Farage declared victory: he has for decades championed leaving the European Union but that was only half of his political double bill.

“The phrase, ‘I’m not racist, but…’ could be invented for some of the things Farage has done in politics,” Tory MP Damian Green said on BBC’s Daily Politics on the day Farage announced his resignation as Ukip’s leader. Stressing he was not accusing Farage of being a racist, Green added: “He encourages feelings that are unhelpful and destructive, and that’s what he’s always done for his political career.”

Farage denies it, leading “Leave” politicians also deny it but in addition to the Ukip fanfare policy of leaving the European Union, Farage and Ukip have unashamedly brought something else to British politics, propagated by the whole “Leave” campaign: xenophobia and outright racism.

The political legacy of the victorious Farage is not only Brexit but the destructive sentiment of xenophobia, particularly appealing to older voters. However, Brexit would never have happened without support from established politicians, most notably Tory politicians like Boris Johnson, Michael Gove, Andrea Leadsom and Labour politicians like Gisella Stewart. With their support, the once so extreme view of leaving the EU, laced with xenophobia, is now mainstream.

The treacherous road from January 22 2013 to June 23 2016

In a speech on 22 January 2013 Prime Minister David Cameron promised to renegotiate UK’s membership of the European Union: no later than 2017 should the British people be given a “simple choice” of a continued EU membership on renewed terms – or leaving the EU.

As so many of his generation in the Tory party Cameron had never shown any particular interest in European matters but the EU has always come handy when a scapegoat was needed: all evil came from Brussels, the brilliance from Tory policies and their leaders.

Given the momentous pledge in 2013, Cameron’s attitude towards the EU was strangely enough no more enthusiastic than earlier. So, after eleven years as a Tory leader and six years as prime minister two months of campaigning didn’t make up for his earlier disinterest in all things European.

At the time of Cameron’s pledge, Farage’s Ukip was enjoying a record following of 10% in the polls, also worrying for Labour. Cameron was not prepared to call a referendum to rid the Tory party of dissident anti-EU ideas and Ukip’s influence.

What Cameron and those around him didn’t seem to understand or didn’t believe was that Ukip’s speak was permeating the mind of so many Tory MPs underpinning not only Brexit but also the other part of the Ukip double bill: the xenophobia and racism. These two currents united in the “Leave” campaign where the political pondus of the likes of Johnson and Gove gave wings to Ukip’s mission.

The “simple choice” of 1975 v the muddled choice in 2016

The seeds for the Brexit disaster were already sown by Cameron when it came to posing the 2016 referendum question: the choice was no longer simple, as it had indeed been in 1975, but a muddled one.

In 1973 the British Tory government led by Edward Heath, decided to join the European Community, a decision tested in a referendum under Labour’s Harold Wilson in 1975; 67% of those voting said yes. Although the motives and arguments were manifold the question – to join or not – was clear and unequivocal.

The recent referendum had a clear “yes” option in the “Remain” but the “no” option, “Leave,” was ambiguous. Wrapped up in the “Leave” was Ukip’s original goal of Britain leaving the EU, never a mainstream opinion in Britain until the referendum – and the stated goal of many Tories inter alia Boris Johnson who argued for his position by claiming Britain would secure a better deal by voting “Leave.”

Bumpy start… towards ashen Tory faces

Farage’s “out” and the “get a better deal” propagated by non-Ukipers gave the “Leave” campaign a bumpy start. Interviews with the Tory “Leavers” waving the “better deal” gave rise to the obvious question what would qualify for a “better deal” leading to unexciting answers.

With the “Take control” slogan things took a better turn for the “Leavers.” Although that also invited convoluted discourse – control of what and what would this new era of British control imply – this slogan could be connected to all relevant issues, be it immigrants or the NHS.

Now, the various sentiments awoken earlier by the fringe Ukip could easily be merged into mainstream Tory speak, useful not only to unruly Tory backbenchers but to leading Tories like Johnson and Gove.

As the voting stations closed June 23 Farage still seemed to believe his long-time apparently so ludicrous goal of pulling Britain out of the EU was lost; seven hours later he was a triumphant if stunned winner.

Contrast Farage’s celebratory appearance with the funeral demeanour of Johnson and Gove when they finally made a public appearance late Friday morning. Their ashen faces indicated they realised they would now need a plan, which they didn’t have. Demagogy and burning ambitions are two sentiments notoriously difficult to harness – a few days later their political fortunes had turned but that is another story.

Farage, leading a fringe party, didn’t feel obliged to have a plan. He had wanted a Brexit, getting it was all he needed to claim victory and he could resign (though given his career of resignations it’s a different matter if he really is leaving politics).

The Ukip xenophobia: from extreme to mainstream

Damian Green’s epitaph of Farage building his political career by encouraging destructive ideas sums up one view of Farage’s political contribution. Farage may fade out of UK politics but his message lingers on among those who took note of his message as they had never before. Not because his message was better or different than it has been for decades but because established and leading politicians adopted and legitimised his stance.

By adopting Farage’s stance on the EU, Brexit supporters like Gove and Johnson, not to forget Andrea Leadsom, also propagated the other part of the Ukip’s political bill, the xenophobia with a whiff of racism. Here, the “Remain” stance of the Labour leadership, especially Jeremy Corbyn, was lamentably weak.

Leading Brexiters from the two big parties vehemently deny xenophobic intentions and undertones but that is too late: thanks to the Brexiters outside of Ukip these views have entered the political discourse. Again, what once was extreme is now mainstream.

The once so loony and laughable

To be exact, this legitimation hasn’t only happened in the last few months. For years, instead of rebutting the often hugely misleading statements from Ukip on immigration with facts and figures established mainstream politicians came to echo the Ukip view. Also, by not engaging the fact that concerns on immigration were the embodiment of simmering anger over political failures since the 1980s was lost.

Already in 2006 Cameron called Ukip “a bunch of … fruticakes and loonies and closet racists mostly.” Like Cameron, established politicians saw Ukip as a crazy fringe party: there was no need to argue with Ukip, no need to correct Ukip-ers’ misleading statements. In the media, largely sympathetic to Ukip’s views, the party was often ridiculed but almost in an endearing underdog way with Farage clowning on BBC’s Have I Got News For You.

With time, there was the seducing option for established politicians to use these sentiments for their own political advantage inter alia by blowing problems with immigration out of all proportions and blaming the immigration on EU rules.

The referendum “Leave” campaign showed that Ukip had by now shaped the immigration debate: further, its views were legitimised by Tory “Leavers” campaigning for a cause earlier only touted by Ukip with arguments earlier only used by Ukip. – This is the grin the parting Farage leaves in British politics.

Danish echoes

The Danish political environment is fundamentally different from the British one but similarly to what has been happening in Britain, xenophobic sentiments, tinged with racism permeated Danish politics in the years up to the elections in 2001. Ukip’s sister party Danish National Party emanating these ideas, jumped from a fringe position with 7% of votes to being the third largest party with 12% of votes and a decisive influence.

In the previous years DNP, founded in 1995 but an offspring of 1970s right-wing currents, had put pressure on the established parties, both the centre-right parties and the Social Democrats, leading many politicians to concede to and echo the DNP view instead of debating it. Buoyed by its 2001 results DNP came to shape Danish immigration policy and the political language: what could earlier not be said had been legitimised. With 21% of votes in the 2015 DNP is now the second largest party in Denmark after the Social Democrats.

Interestingly, in Denmark immigration hasn’t been blamed on EU but been a domestic bone of contention. In spite of sceptic EU-attitude there is no appetite in Denmark to leave the EU and hasn’t been for years. DNP, which used to be anti-EU has without fanfare abandoned its anti-EU stance.

There is however a Danish Brexit effect: opinion polls show increased support for Danish EU membership and less appetite for a Danish referendum on membership. Before the British referendum 40% of Danish voters wanted a referendum on Danish EU membership, 60% preferred to stay in the EU and 22% wanted to leave; now these numbers are respectively 32%, 70% and 18%.

Abdicating political responsibility

When David Cameron, under pressure from Ukip, promised a referendum he might have been lured by an easy game against “loony fruitcakes.” Following an albeit narrow win in the 2014 Scottish referendum and in the 2015 general elections he lost the EU referendum and together with that loss, xenophobia and worse has come to stay in British political debate.

The economist Joseph Schumpeter (1883-1950) claimed the welfare system would be in danger when the sense of entitlement to gain from it was greater than the will to contribute to it. Similarly, democracy is in danger when politicians take it too much for granted and can’t be bothered to argue with ideas that undermine it. After all, being in power means not only having power to take action but also to sway and influence opinion.

Cross-posted on A Fistful of Euros.

Follow me on Twitter for running updates.

Let them litigate

“Iceland’s selective default?” was the topic of a seminar in New York this week, organised by EMTA, the association of emerging markets investors. The measures taken by the Icelandic government and the Central Bank to reduce the offshore króna have placed the question mark in the question. Sadly, that question mark was not erased at the meeting but that doesn’t seem to worry the Icelandic government.

The concept selective default has been waved around recently in connection with the measures taken by the Icelandic government: at the strategic time, just before – what is or was to be – the last offshore króna auction, two foreign experts waved the “selective default” banner in Wall Street Journal and FT Alphaville (see my latest on this).

The two writers were present at the EMTA event in New York, James Glassman as the moderator, with Arturo Porzecanski on the panel together with Magnús Árni Skúlason, an Icelandic economist advising some of the funds holding the offshore króna and Lee Buchheit from Cleary, Gottlieb, advising the Icelandic government.*

Very much contrary to how the estates of the failed banks were dealt with last year (as I have repeatedly pointed out) – when nothing was finalised until the creditors had agreed to the measures – the Icelandic government, advised by Cleary, is engaging with offshore króna holders, to use an Icelandic expression, “with two ram’s horns,” meaning belligerently. Or as Buchheit said: let them litigate.

It is indeed a real possibility that the largest funds will litigate their way through this mess. The question is what that would entail for Iceland in terms of inter alia long-lasting and costly litigation, negative effect on credit ratings and possible delays in lifting capital controls, the goal of the whole exercise. In addition, several interesting points came up in the debate: the banks’ estate v offshore króna; recent restrictions on inflows; discrimination based on nationality – and was the recent auction really the last one?

Litigation: a real threat?

Icelandic authorities have deemed the auction successful because of good participation although CBI governor was more cautious. True, there were plenty of bids – but small ones. The large offshore króna holders didn’t participate or their offers weren’t accepted. Ergo, the bulk of the offshore króna is still inside capital controls. There is now litigation in the air, the largest offshore króna holders, all large international funds, have taken the first steps in that direction. The question is what the effect on Iceland and the Icelandic economy will be.

Buchheit said he wanted to puncture what the articles by Glasman and Porzecanski stated. He dismissed that the offshore króna holders had any claim on the Icelandic sovereign. Waving a dollar note, he stated that owning this note didn’t make him a creditor to the US; equally, owning a króna didn’t make the offshore króna holders a creditor to the Icelandic sovereign. – However, the large offshore króna holders aren’t waving króna bills but Treasury securities; around 2/3 of the offshore ISK319bn are Treasury securities which makes the situation slightly more convoluted.

Dismissing any comparison with Argentina, Buchheit did however neither directly counter the argument that the underlying assets are indeed Treasury securities nor give any tangible argument against the Argentina comparison except claiming it was not true. The funds could try litigating but neither Britain nor the Netherlands had found great sympathy for their cause, he said.

This must refer to the Icesave dispute, ruled on by the EFTA Court in January 2013 (link to the Judgement and my digest of the main points.) From the point of view of Iceland this seems a worryingly feeble argument since that dispute was, as far as I can see, fundamentally different from the issues at stake re the offshore króna (see below). Also, the argument that the offshore króna holders had bought their assets with a haircut inside capital controls seems beside the point; the point is that an owner of these securities can demand a payment on time and in full.

The testing point will be if courts – in Iceland and possibly elsewhere – will side with offshore króna holders or not. After all, Argentina decided to negotiate with those holding Argentinian sovereign bonds after a costly dispute lasting 15 years where Cleary Gottlieb was their main adviser (but not Buchheit until at the recent and final negotiations).

Cooperation last year, none this year

It now seems that the Icelandic strategy is to fix the offshore króna overhang with this last auction with remaining funds placed on locked low-interest accounts with the CBI, as the Treasury securities reach maturity, thus ignoring the possible legal risk. The next steps will then be towards lifting controls on the domestic economy, most importantly the pension funds. Only later will the locked accounts be revisited.

Magnús Árni Skúlason stressed that the funds he advised had come up with many proposals as to how to solve the issue. He pointed out that due to the very strong and booming Icelandic economy and sizeable foreign currency reserves it was difficult to argue for a haircut on grounds of a weak economy.

As I’ve repeatedly pointed out I find the difference in approach last year with the creditors of the failed banks and now with the offshore króna holders perplexing. In the latest IMF Article IV Consultation with Iceland, concluded on June 20, the IMF compares its 2014 recommendations with Authorities’ responses. On capital controls the IMF recommended in 2014 that the “updated liberalization strategy should be comprehensive, conditions based, and with an emphasis on a cooperative approach with appropriate incentives.”

As to the Authorities’ response the “updated liberalization strategy released in June 2015 takes a staged approach. The bank estates were resolved first, in a cooperative manner, which minimized legal and reputational risks and won credit rating upgrades. The authorities are now working to release offshore króna investments via an auction. Residents will be addressed thereafter (emphasis mine).

Minister of finance Bjarni Benediktsson has earlier emphasised the same as the IMF above, as did Buchheit at the EMTA meeting, that creditors have not challenged the measures last year in lifting capital controls on the banks’ estates. Due to the “cooperative manner” last year there were no legal challenges, which again raises the question why it’s suddenly not important to avoid the legal and reputational risk. So far, no clear answer.

Misconceptions on Icelandic “vindictiveness”

In his FT Alphaville guest blog Arturo Porzecanski criticised the Icelandic government for its measures on offshore króna, pointing out that the measures would place Iceland in selective default. He also strongly criticised recent law authorising the CBI to impose measures to discourage foreign inflows into Iceland.

Porzecanski embellished his points further at the EMTA meeting. According to him, the Icelandic government is, in his words, being “vindictive;” as if investors were responsible for the 2008 crisis, the government now wanted to “bleed investors” as it had tried last year with what he called a “departure tax” on creditors of the failed bank. However, he didn’t mention that the outcome an agreement with creditors (see my blog). To him this all smelled of punitive coercive action, just as in Greece and Argentina.

The tone in Iceland towards foreign investors has at times been harsh, mainly because of the politics at play, but Porzecanski’s description is to my mind out of proportions. After all, a 2010 report by an Icelandic Special Investigative Commission on the 2008 banking collapse, firmly and squarely placing the responsibility with Icelandic authorities, the CBI and politicians. And Icelandic bankers have been sentenced to imprisonment for criminal actions before the collapse of the banks.

The measures to temper inflows have long been expected: already in 2012 the CBI published a report on Prudential Rules Following Capital Controls, outlining what is needed to preserve financial stability once the capital controls have been lifted. Quoting IMF research one of the measures announced is restricting inflows, as indeed many countries have done over the past decades.

Porzecanski claims this is just done because the inflows were seen as a problem earlier, saying there is no justification for this measure. Well, he is right that the inflows were seen as a problem earlier, indeed the capital controls were put in place with the blessing of the IMF because of inflows, now the offshore króna overhang. As Porzecanski should be aware of and as emphasized in the 2012 report, IMF research underpins these measures, as do many economists. From the publication of the 2012 report it was clear that in due course these fairly traditional restrictions would be made use of.

Discriminating between foreigners and Icelanders?

A question from the audience at the EMTA event, on potential discrimination between Icelanders and foreigners, raised some interesting issues. The point was that Icelanders holding a króna would get a full króna whereas the offshore króna measures subjected foreign króna holders to getting only say 70 aurar (100 aurar = 1 króna). Buchheit’s point was that there was no discrimination involved. – Yet, the question still raises an interesting aspect.

The Emergency Law, passed on 6 October 2008 did differentiate between deposits held by individuals and entities domiciled in Iceland and abroad (which has partly shaped the definition of the offshore króna). This division was in fact a version of splitting the banks into a bad and good bank since roughly the foreign loans were put into the estates and Icelandic deposits into the new, living banks (it was slightly more complicated but this is the rough outline). – The Emergency Law has been contested in Icelandic courts and found to be in accordance with the constitution and Iceland’s international obligations.– These were extreme measures in extreme time taken by a sovereign defending its vital interests.

Eventual discrimination came up also in the Icesave case as the EFTA Surveillance Authority claimed in the EFTA Court, focusing on the use of the Icelandic Deposit Guarantee Fund, TIF. The question of discrimination was deflected in the Judgement due to the course of events in Iceland: the deposits had indeed been moved from the failed banks to the new banks but not reimbursed by the Icelandic TIF. Consequently, the Icelandic TIF didn’t need to reimburse foreign depositors, i.e. there was on discriminations involved and no breach of the relevant Directive. – Maybe it’s my lack of legal intricacies but I don’t quite see the relevance of the EFTA Court Icesave Ruling for the offshore króna problematic (as above, link to the Judgement and my digest of the main points.)

Is this really the last auction – and more confusion

In his introductory remarks Buchheit mentioned offhandedly that there are FX auctions all the time and this latest one was just another auction, in a series of 22 offshore króna auctions. Porzecanski asked if this meant this latest really was just another auction, would there be auctions following this announced last one but got no answer.

Porzecanski also pointed out that this last auction was indeed not a proper auction, more like bringing work of art to an auction house which then would set the price, i.e. no bidder on the other side.

During the question and answer session Skúlason mentioned that one concern of his was that part of the underlying assets was indeed Treasury bonds. Buchheit agreed there were some bonds, which would be paid in full and on time as Iceland had a stainless record in terms of fulfilling its sovereign obligations: it has never defaulted. – This statement seems to conflict with earlier statements – unless there is some tricky teleological interpretation behind the advice to the Icelandic government.

Last year, my main worry regarding the estates of the failed banks was if the government was ever going to have the political strength to agree on the necessary measures (mainly the haircut of the estates’ króna assets) and secondly that these measures would steer clear of legal risks. This year, the worry is that for some inexplicable reasons the cooperative method isn’t in vogue, in Iceland, possibly leading to legal risks and reputational damage so astutely avoided last year. Maybe I’m missing something but the discussions at the EMTA meeting didn’t inspire much confidence: “let them litigate” sounded decidedly belligerent compared to the cooperative approach last year.

*I had been invited to join the panel but ended up only listening via phone from London.

Follow me on Twitter for running updates.

An auction that didn’t solve the problem and the past as an aberration

The outcome of the offshore króna auction 16 June has now been made public: offers at the rate of ISK190 a euro or lower were accepted. According to the Central Bank of Iceland press release a “total of 1,646 offers were submitted and 1,619 accepted; however, these figures could be subject to change upon final settlement. The amount of the accepted offers totalled just over 72 b.kr., out of nearly 178 b.kr. offered for sale in the auction.” – The on-shore rate is ISK139 to the euro. The question is how credible this outcome is, given the good economic conditions in Iceland. (Further to the background see an earlier Icelog here).

Although the auction apparently was a final offer the CBI is now offering to “purchase offshore króna assets not sold in the auction at the auction exchange rate of 190 kr. per euro.” The terms and conditions will be published tomorrow with the deadline at 10 o’clock this coming Monday morning, 27 June. The finale outcome of the 16 June auction and potential transactions in the following days, until Monday morning, will be published that Monday with settlement of both transactions completed on that day.

This outcome is far from the stock of ISK319bn that the offshore króna amounts to. The auction was supposed to be the last in a series of 23 auctions; this offer to buy offshore króna at the auction price of ISK190 is now a tail to that last auction.

In an interview on Rúv tonight, CBI governor Már Guðmundsson said that out of 1,646 offers submitted 1,619 had been accepted, or 98%. This means there are now a whole lot fewer offshore króna holders left – but the problem is, as Guðmundsson rightly acknowledges, that all the big funds holding these assets are holding on to their króna. “It is clear that the rather big holders have either not participated or offered a rate we could not accept,” said Guðmundsson.

In a cage – at the back of the queue

The governor said that with the auction out of the way, capital controls can now be lifted on domestic entities and individuals, i.e. Icelandic companies, pension funds etc. The process has been designed in such a way, according to Guðmundsson “that those who do not leave now stay in a similar financial environment as they have been in so far as to investment offers with added changes, which were necessary to secure that this environment would be stable even if we lift controls on domestic entities. They (i.e. the offshore króna holders) will now go to the back of the queue, they were at the front and then at some point it will again be their turn.”

This is undoubtedly a description the big offshore króna holders will contest. They will claim that conditions have been seriously tightened. When their assets mature these assets will automatically go into deposits at 0.5% interest rates, effectively negative interest rates, held with the CBI, very much akin to the cage that Guðmundsson once described so vividly at a meeting in Iceland.*

Thus the big offshore króna holders, who did not participate (or offered a non-accepted rate) will now feel they are in a cage at the back of a queue not knowing when they will be released. Or in other words: they will claim that the sovereign isn’t paying back its loans.

Calling things their right names

What is it called if a country pays only some of its debt? The term is “selective default” – and worryingly that’s now the term attached to Iceland if offshore króna holders, where Icelandic sovereign bonds and T-bills are the underlying assets, are not paid out in full.

Offering a rate of ISK190 to a euro when the on-shore rate is ISK139 in a country doing pretty well seems like a drastic haircut – and it is incidentally involuntary, from the point of view of the offshore króna holders, although the Icelandic government claims there was a fair second offer, i.e. the cage at the end of the queue.

In a defiant answer to a WSJ op ed, minister of finance Bjarni Benediktsson rejects that Iceland can be compared to Argentina. However, he fails to point out that after fighting creditors for fifteen years Argentina did indeed finally settle with creditors. A country can claim as much as it wants that it’s honouring all its obligation but the arbiter is not the country itself but the International Swaps and Derivatives Association, ISDA, which decides on which events release credit default swaps.

Reputation risk

I have earlier talked about the mixed messages from Iceland in dealing with creditors. Last year, great care was taken in negotiating with creditors when it came to lifting capital controls on the estates of the three collapsed banks.

This time, when the sovereign is directly involved, contrary to last year, the strategy is to offer a cage at the back of a queue with no date as to when that backend will be served. There must be a strategy somewhere but I can’t see it, which is worrying since the outcome could be lengthy court cases in all and sunder jurisdictions for years to come. In the world of short-term politics that would inevitably be a problem for another day and another government.

In the meantime, the financing cost of all things Icelandic, whether state or private sector, will either go up or stay as it is, instead of going down as it well could soon with the bright economic prospects there are (and as Moody’s had already beckoned). This was kept in mind last year. Now it seems that this past of playing carefully was not a prologue to the present but an aberration. Consequently, Iceland might be back to a costly future of reputation risk.

*At a public meeting on the offshore ISK in 2013, some of those present argued that the solution to the Icelandic current account problem was just to cage in the foreign-owned assets so capital controls could be lifted on the domestic part of the economy. Present at the meeting was CBI governor Már Guðmundsson who pointed that when new investors would then arrive in Iceland they would see the cage and ask who was in it. “The investors who invested in Iceland last time around.” (From an earlier Icelog).

Update: This morning, Wed. 22 June, minister of finance Benediktsson talked at Euromoney Global Borrowers and Investors Forum where I interviewed him afterwards; Benediktsson claimed the offshore króna auction had been a success in terms of the many bids received and now those remaining would have to wait. He said there had been no legal aftermath following the composition of the estates last year, precisely because it had been well prepared but said he was not worried this time. It was to be expected that the hedge funds holding offshore króna were making a noise but that was nothing the minister was worried about.

Follow me on Twitter for running updates.

Mixed messages from Iceland

While the Icelandic government is planning to play clever and give offshore króna holders, i.e. sovereign bondholders, a haircut – apparently because the Icelandic economy isn’t strong enough – Kaupthing, the largest owner of Arion bank , and that bank are assessing how to make use of the strong Icelandic economy with regards to Kaupthing’s shares in Arion. An intriguing case of “mixed messages”… now that another step is being taken to further ease the capital controls, in place since November 2008.

In the past few days, two articles have appeared – an op ed in Wall Street Journal and a guest blog on FT Alphaville – spelling out that Iceland is about to opt for a sovereign default, quite voluntarily and apparently with open eyes.

Iceland, of course, doesn’t quite see it that way, as I explained recently at some length. That said, I have been utterly baffled why Iceland, having taken such care last year to avoid all legal risk by negotiating with the creditors of the three fallen banks, is now reverting to the tactic, which at the time of the collapsing banks in October 2008 was half (but not quite) jestingly called “xxck the foreigners.”

Last year, some foreign pundits were comparing Iceland’s situation with Argentina, a wholly misplaced comparison since the government was no partner to the composition of the estates of the banks though the government had to take on the role of a facilitator in solving problems related to the foreign-owned, i.e. offshore ISK assets of the estates.

The outcome was around 75% haircut of the Icelandic assets. So successful was this step towards easing capital controls that foreign inflows into sovereign bonds started at once, now amounting to around 5% of GDP – nothing compared to the 44% of GDP in November 2008 when the capital controls were put in place, under the auspice of the International Monetary Fund.

This time the government IS the other party since the offshore ISK assets are sovereign securities, which led James Glassman in the WSJ and then Arturo Porzecanski* in FT Alphaville to compare Iceland to Argentina: Iceland was about to turn into a very chilly version of Argentina.

Actually, after years of legal wrangling Argentina has of course finally settled with creditors, advised by the law firm Cleary Gottlieb, also advising Iceland (though somewhat ominously Cleary was the adviser not only in solving the Argentinian problem but also during the dark years); Argentina is now happily borrowing again. Financial firms have a notoriously short memory, after all they can’t afford to hold grudges. But the legal wrangling all over the world did blight the lives of Argentinians for around 15 years and no need to minimise how unpleasant and costly it all was.

The Icelandic situation right now is that tomorrow, on June 16, the Central Bank of Iceland will hold an auction for OS ISK holders (all info here). After setting the terms in such a way that a hair cut was all but inevitable for those participating in the auction and negative interest rates for those who didn’t the terms were changed this week – last minute wisdom… or panic, depending on the reader:

The amendments to the Terms of Auction removes ambiguity about whether, in spite of the auction results, the Bank can decide on a more favourable auction price than is specified in the table. As before, all owners of offshore krónur will receive the same price for their krónur, as the auction has a single-price format, which applies irrespective of whether the price accepted is lower than is specified in the table. It is appropriate to reiterate that as before, the Central Bank reserves the right to accept some or all of the offers submitted, or to reject all of them (emphasis mine).

Effectively, the CBI can now choose to accept the best offer… or well, come up with a better one.

Two questions: why this sudden and very late change and why was such care taken last year to negotiate whereas now it’s a take it or leave it offer?

As to the sudden change I don’t know but given the fact that a high participation is needed to solve the issue – or otherwise the OS ISK will be locked up in a really cold dungeon, i.e. at negative interest rates with no maturity in sight but only some vague words of a revision when suitable – it can be surmised that the CBI sensed that the large OS ISK holders were not going to participate: they have indicated as much. Although the auction is set for June 16 this isn’t the kind of auction where bidders walk in from the street and wave their hands; the bids will have been placed earlier due to time-consuming procedures.

On the different approach last year v now I had already made some guesses in my last blog: whetted appetite for collecting more for the state coffers, following last year’s windfall from the estates’ ISK assets; political need for a victory before the planned election in October (no date set yet); the certainty that OS ISK owners can’t rely on Icelandic courts to rule in their favour against the sovereign; using the harsh terms as a stick to beat the ISK holders (but when?) – I don’t find any of these very plausible, partly because I don’t see any of these reasons as a winning strategy.

One lesson from the Argentina very very long struggle is that international creditors rely on a many-pronged strategy, i.a. legal actions not only in the home country of the bond issuer but in many jurisdictions. I refuse to believe that Icelandic courts would side with the sovereign against the law but ultimately that’s not a deciding point since legal action will, most likely, be taken in many jurisdictions. And it’s not up to Iceland to define if a certain action is a default event or not.

The fact that two non-journalistic articles have already been published in international finance media indicates interest in certain quarters and a preparation, meaning that the large OS ISK holders, quite unsurprisingly, already have their plan A B and C mapped.

Considering the strong Icelandic economy Iceland has in general a weak case for forcing a haircut on holders of Icelandic sovereign bonds. The government can certainly hold its course but testing its limits to such a degree that it loses control of the situation – as it would i.a. if legal action were taken against it – shows at best lack of realism and worst a staggering stupidity.

That brings me to the same question as earlier: after the care taken last year to avoid time consuming action and legal risk why is the government and the CBI now opting for a course that involves all the things religiously avoided last year?

*In his blog Porzecanski is dismayed that the CBI and the government have recently passed a Bill to temper inflows. This action does however not come as any surprise. Already in its 2012 outline of prudence rules following the lifting of capital controls the CBI spelled out various measures which would be used in the future to secure financial stability. Considering the fact that the inflows in the years up to 2008 ultimately caused Iceland to opt for the capital controls, now being eased, this prudence is highly sensible, in my opinion. Yes, interest rates could be lowered in order to temper the appetite of international investors but that’s another thought for another day. In short, I definitely don’t share Porzecanski’s view though I can see his point. There is an Icelandic saying that a burnt child stays away from the fire – and that is, I’m sorry to say, an apt description of the mood in Iceland re foreign inflows.

Updated: Minister of Finance Bjarni Benediktsson has now responded in the Wall Street Journal, claiming that Iceland shares little with Argentina except that creditors have bought distressed debt at knock-down prices. – However, in the end it only matters who holds the debt, not how it was acquired. Also, Benediktsson does not mention that after legal wrangling, at great cost also legal cost, over 15 difficult years Argentina did indeed negotiate with creditors.

Follow me on Twitter for running updates.

Capital controls and legal risks: major concern last year, ignored now

In the months leading up to the June 2015 plan on moving the three banking estates out of capital controls minister of finance Bjarni Benediktsson was adamant about avoiding legal risk. Indeed, that plan was only announced once the creditors had agreed to a haircut on the estates’ króna assets. The new Act on the offshore króna raises some legal issues as two of the four funds holding the lion share of these assets have pointed out in a letter to Alþingi. Intriguingly and contrary to last year, Benediktsson and the Central Bank of Iceland now seem to be intensely relaxed about legal risk though this time, contrary to last year, it really is the state that is the counterparty.

There has been little debate in Iceland regarding the offshore ISK and measures to lift controls on its owners. Certainly, the numbers are fundamentally different from when these offshore ISK, i.e. owned by foreigners (individuals or entities registered abroad; can in theory be Icelandic and are in some cases) caused the introduction of capital controls in November 2008. At the time these assets amounted to 44% of Icelandic GDP; now they amount to 14% of GDP or ISK319bn.

The largest part of the offshore ISK is owned by a few large institutional investors, two of them being Autonomy Capital and Eaton Vance. The underlying assets are Icelandic sovereign bonds and T-bills, meaning that the counterparty here is the Icelandic state.

As with creditors last year there have been meetings between the large offshore ISK owners and Icelandic representatives of the ministry of finance and the CBI. Contrary to last year, when nothing was done until it had been negotiated with the creditors of the estates, no agreement was reached before the new Act was passed in parliament this weekend.

Officials met with representatives of offshore ISK holders yesterday in New York to inform them of the new measures.

The state sure will pay its debt or… maybe not

Last year, creditors to the estates agreed to roughly a 75% haircut on the estates’ ISK assets. This outcome came as no surprise but had been more or less foreseen for the last several years, based on the Icelandic current account: this is what Iceland could manage without upsetting financial stability.

Hawkes among Icelandic officials have been adamant that offshore ISK owners should endure a similar fate. That however goes against the rule that a state pays its debt in full. At a hearing in the parliament’s economy and trade committee a CBI official underlined this fact: the sovereign will pay its debt.

This is clearly what the funds owning the offshore ISK have literally been banking on: the state is its counterparty and a state pays its debt.

Two options: ISK220 for a euro or deposit at negative rate

The new Act (English translation of the Bill) stipulates that offshore ISK holders can participate in an auction where the reference exchange rate will be ISK220 for the euro, more than a third higher than the present onshore rate of ISK140.

There was a meeting in New York yesterday, where the measures were explained. Clearly, a higher participation in the auction would lead to a better price (creating a version of “prisoner’s dilemma”…) but the funds might also calculate that they were better off heading to court.

If an auction doesn’t tempt them the assets will be turned into a “Central Bank of Iceland certificates of deposit: Debt instruments issued by the Central Bank of Iceland to deposit money banks that hold offshore króna assets in accounts subject to special restrictions.” This debt instrument has no maturity, interest rates are set at 0.5% but will be reviewed annually. Needless to say, 0.5% in Iceland is negative interest rates, well below inflation.

Effectively, the offer is either a haircut of more than a third of the assets or a lock-in at negative interest rates for unspecified time.

If the haircut was meant as a carrot compared to the lock-in stick, offshore ISK owners might well keep in mind the CBI official’s words that the sovereign was of course going to pay its debt in full – and simply head for the courts.

Property rights and human rights

Over the weekend, Eaton Vance and Autonomy sent a clarification of their stance to parliament (here, in Icelandic). The funds protest the Bill defines all offshore ISK as being “potentially more volatile than other króna-denominated assets, as the latter are subject to a home bias.” This does not at all apply to the funds, they claim since they have already shown a preference to being long-term investors in Iceland, i.e. they are willing to buy Icelandic bonds and T-bills.

In addition, they point out that considering growth and good state of the Icelandic economy, the present offer can’t be justified by hardship, as emergency measures following the banking collapse in October 2008.

Furthermore, the funds see their position as being strong since a partial payment would amount to a credit event, thus putting the state into default, with all the unpleasant consequences involved – a potentially expensive experience for Iceland, both the state, public institutions and companies.

There is a “Provisions of the Constitution and the European Human Rights Convention” in the Bill, stating that the “recommendations in the bill of legislation have been drafted with the aim of maintaining compliance with the Constitution and the European Human Rights Convention, particularly as regards protection of ownership rights and prohibition of discrimination.” – The funds clearly disagree and consider these provisions to be inadequate.

A legal risk but so what…

One view heard from one of those involved on the Icelandic side is that the measures are clearly close to the margin of the possible and postulate a clear legal risk. However, there was no need for Icelandic authorities to pay any special attention to problems the offshore ISK holders might identify, according to this source. Yes, the offshore ISK owners could now decide to challenge the Act but perhaps they had already had enough of wrangling with Icelandic authorities and might just be ready to call it a day. And anyway, an Icelandic court is unlikely to rule against the parliament, states the source.

That is certainly one way of seeing the situation. What I find difficult to explain is why the minister of finance and other officials were so adamant last year about avoiding all possible legal risks, by beforehand securing the creditors’ support to the plan to lift controls for the estates – but are now apparently intensely relaxed about possible legal risks and the pretty obvious invitation to a legal challenge.

All the more surprising since the creditors to the estates had known for a long time that they would only get part of their ISK assets whereas the offshore ISK owners are certainly counting on the state paying back and in full.

Could the Act be only a stick (as was the “stability tax” last year), are talks still going on? That’s one version and an Act of law can certainly be changed. That said, I still find the Act looking surprisingly like a final act if the intention is to explore further avenues with offshore ISK holders.

Reputation risk and “those in the cage”

At a public meeting on the offshore ISK in 2013, some of those present argued that the solution to the Icelandic current account problem was just to cage in the foreign-owned assets so capital controls could be lifted on the domestic part of the economy. Present at the meeting was CBI governor Már Guðmundsson who pointed that when new investors would then arrive in Iceland they would see the cage and ask who was in it. “The investors who invested in Iceland last time around.”

This doesn’t seem to be the most alluring introduction to Iceland but that is none the less what seems about to happen: offshore ISK holders are being offered a cage, unless they prefer fleecing.

Icelandic officials will clearly have Icelandic interests at heart. Last year, it seemed that these interests were best safeguarded by negotiating an outcome with creditors so as to secure a full harmony in the outcome and execution. With the offshore ISK the same officials seem to act in the certain belief that the state can dictate an outcome it wishes, with no need to pay any special attention to those who lent money to the state and who are also willing to continue lending. It will take some time before it’s clear if this is a sound judgement and what the possible reputation risk will be.

Update: here is further information from Ministry of finance on the new Act.

Follow me on Twitter for running updates.