Archive for July, 2016

Next step by offshore króna holders: call the IMF

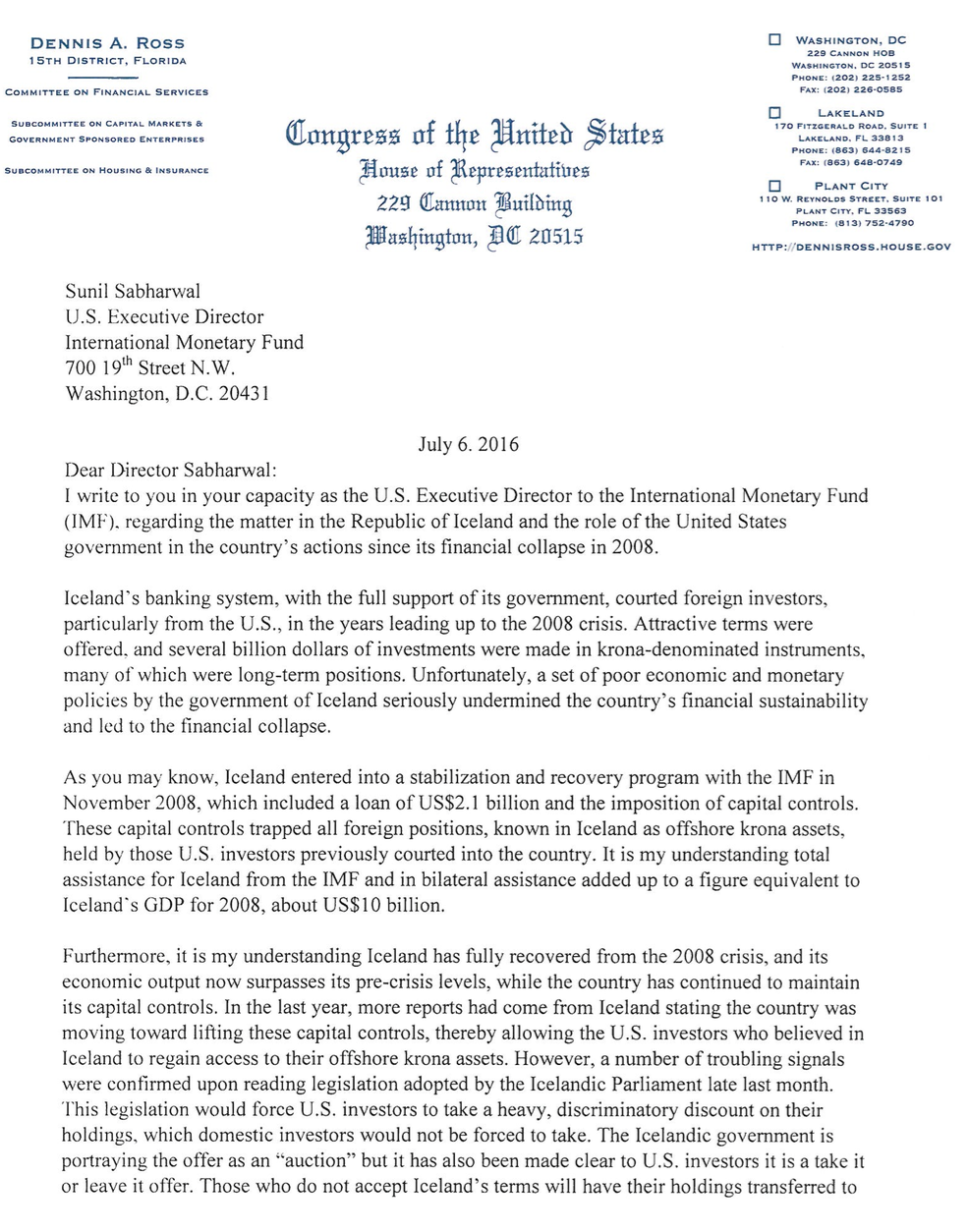

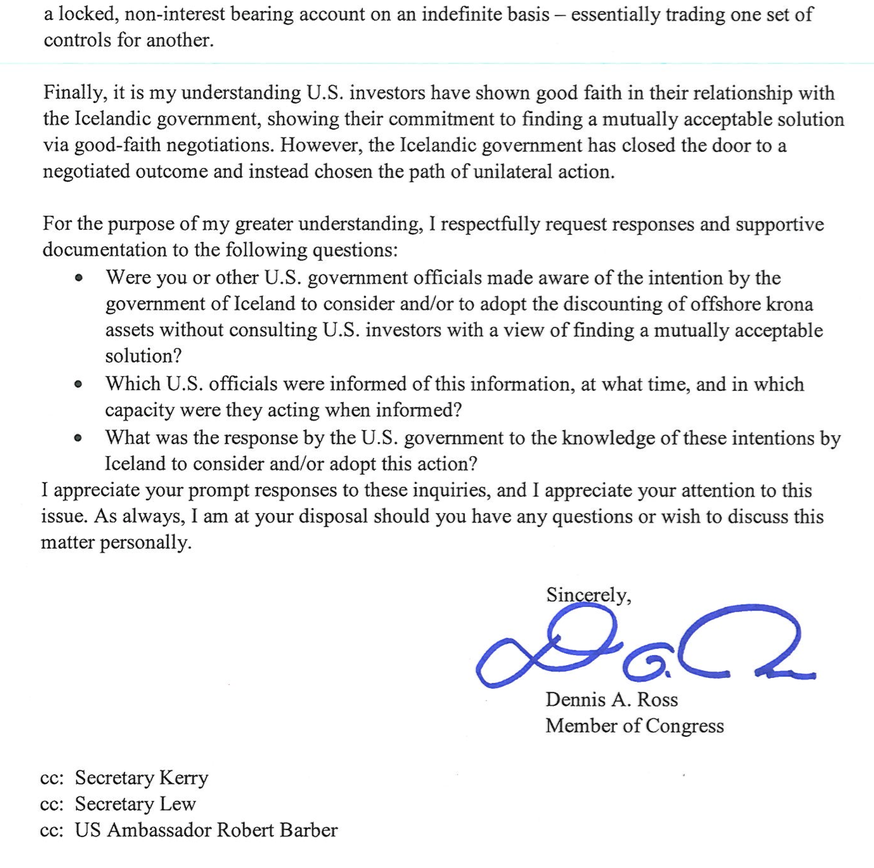

Congressman Dennis A Ross has written a letter, see below, to Sunil Sabharval, US Executive Director at the International Monetary Fund, IMF, inquiring as to what US officials knew about the offshore króna actions taken by the Icelandic government. The Congressman’s mission is clearly to safeguard US interests, i.e. the interest of US funds holding offshore króna, a problem I have dealt with extensively in earlier blogs, inter alia here. Although not stated explicitly, the most sensitive underlying assets are sovereign securities, payable in Icelandic króna.

In the letter the reasons for the Icelandic collapse are somewhat simplified to say the very least, apparently easier to blame the government than the banks; also rather funny to see the offshore króna holders treated as entirely blameless lured by good deals, another saga.

The thrust of the letter is that since Iceland has now recovered well from its 2008 crisis Iceland shouldn’t be discounting the offshore króna or offering the investors punitive terms. – Further to this: intriguingly, Iceland had not made a loss on the 2008 banking crisis but a gain of 9% of GDP(!), according to the latest IMF Article IV Consultation statement on Iceland, from June 22.

The Congressman points out that the offshore króna holders (i.e. the largest holders) have come up with various solution but Icelandic authorities have been unwilling to take any notice. He now wants to know if US officials are aware of what is going on – and he expects an answer, which as far as I know has not yet been given. IMF has preached a cooperative approach to lift capital controls, reiterated in its June statement on Iceland but seems to consent with the action taken by Icelandic authorities re the offshore króna.

Here is Congressman Ross’ letter:

Last time, this time – in general

As I recounted at length in the years, months and days up to the plan to lift capital controls on the estates of the banks, presented June 8 last year, Icelandic authorities dithered for long due to infighting until they took the plunge – to be fair, the authorities claimed it just took time to prepare the plan and refused all allegations of infighting. But the plunge wasn’t taken until it was clear the plan was supported by the largest creditors.

The same now with the offshore króna action, it all took longer than had been planned, my understanding is that it took long because of different views; however, those involved say it just took the time it took, complicated matters etc. Yet, this time the government acted unilaterally, no agreement with the largest offshore króna holders. Thus inter alia the above letter, I assume.

The government claims the offshore króna holders do not act as a group, contrary to the creditors to the old banks. That isn’t wholly correct – each estate had to be dealt with separately and support was sought for each estate. Thus, the creditors were not a unified group but three groups. So much for that argument now re the offshore króna holders.

As a ground for pride Bjarni Benediktsson minister of finance has pointed out that there was no legal aftermath to the plan last year. Quite true but that’s because the plan wasn’t passed until creditors’ support was ensured. Which is exactly the opposite of now where the government has acted unilaterally re the offshore króna holders who consequently have taken the first steps towards legal action.

In addition, there is the concern Congressman Ross shows, as well as articles in the Wall Street Journal and FT Alphaville, as I have mentioned in earlier blogs – offshore króna holders are clearly trying to point out to the world that Iceland, by planning a haircut on the offshore króna assets (when they are converted into foreign currency) doesn’t intend to honour its international commitments.

Last time, this time – in particular

I have earlier pointed out that I was wondering if the Icelandic government was going to make use of some “tricky teleological interpretation” in its dealings with offshore króna holders.

I didn’t explain in any detail what I had in mind but here it is:

Long before the June 8 plan last year, the Icelandic government claimed it couldn’t possibly have anything to do with the composition of three private banks. Right, except that composition was meaningless if it wasn’t clear beforehand how much of the Icelandic assets creditors (only 10% of the assets went to Icelandic creditors, mostly the CBI) could convert into foreign currency. Composition agreement couldn’t be reached until the government had found a solution i.e a haircut, which the creditors could agree to – that was what mostly took so long to solve.

This time, the core of the offshore króna problem is similar regarding sovereign securities. The government can claim that it’s honouring all its obligations as it will pay out any such securities in full and on time… in króna. The thing is that offshore króna holders can – or could, the auction is now over – either choose to convert at ISK190 a euro (the onshore rate is now ISK136, was ISK139 at the time of the auction) or have their króna kept on a special deposit account at 0.5% interest rates with no maturity in sight. The question is if this is seen as fair… or not.

Last year, the government came to the conclusion that it had to step in to facilitate a composition. Now, it’s just shrugging its shoulder and the message is, as I’ve stated earlier, “let them litigate” – alors, last year, the goal was to prevent legal action, this year it’s bring it on…

Follow me on Twitter for running updates.

Ukip’s sinister double bill and failed political leadership

Until early this year it seemed unlikely that an extreme idea lingering for two decades on the political fringe could turn into a mainstream choice preferred by majority of British voters as happened on June 23. Ukip’s leader Nigel Farage declared victory: he has for decades championed leaving the European Union but that was only half of his political double bill.

“The phrase, ‘I’m not racist, but…’ could be invented for some of the things Farage has done in politics,” Tory MP Damian Green said on BBC’s Daily Politics on the day Farage announced his resignation as Ukip’s leader. Stressing he was not accusing Farage of being a racist, Green added: “He encourages feelings that are unhelpful and destructive, and that’s what he’s always done for his political career.”

Farage denies it, leading “Leave” politicians also deny it but in addition to the Ukip fanfare policy of leaving the European Union, Farage and Ukip have unashamedly brought something else to British politics, propagated by the whole “Leave” campaign: xenophobia and outright racism.

The political legacy of the victorious Farage is not only Brexit but the destructive sentiment of xenophobia, particularly appealing to older voters. However, Brexit would never have happened without support from established politicians, most notably Tory politicians like Boris Johnson, Michael Gove, Andrea Leadsom and Labour politicians like Gisella Stewart. With their support, the once so extreme view of leaving the EU, laced with xenophobia, is now mainstream.

The treacherous road from January 22 2013 to June 23 2016

In a speech on 22 January 2013 Prime Minister David Cameron promised to renegotiate UK’s membership of the European Union: no later than 2017 should the British people be given a “simple choice” of a continued EU membership on renewed terms – or leaving the EU.

As so many of his generation in the Tory party Cameron had never shown any particular interest in European matters but the EU has always come handy when a scapegoat was needed: all evil came from Brussels, the brilliance from Tory policies and their leaders.

Given the momentous pledge in 2013, Cameron’s attitude towards the EU was strangely enough no more enthusiastic than earlier. So, after eleven years as a Tory leader and six years as prime minister two months of campaigning didn’t make up for his earlier disinterest in all things European.

At the time of Cameron’s pledge, Farage’s Ukip was enjoying a record following of 10% in the polls, also worrying for Labour. Cameron was not prepared to call a referendum to rid the Tory party of dissident anti-EU ideas and Ukip’s influence.

What Cameron and those around him didn’t seem to understand or didn’t believe was that Ukip’s speak was permeating the mind of so many Tory MPs underpinning not only Brexit but also the other part of the Ukip double bill: the xenophobia and racism. These two currents united in the “Leave” campaign where the political pondus of the likes of Johnson and Gove gave wings to Ukip’s mission.

The “simple choice” of 1975 v the muddled choice in 2016

The seeds for the Brexit disaster were already sown by Cameron when it came to posing the 2016 referendum question: the choice was no longer simple, as it had indeed been in 1975, but a muddled one.

In 1973 the British Tory government led by Edward Heath, decided to join the European Community, a decision tested in a referendum under Labour’s Harold Wilson in 1975; 67% of those voting said yes. Although the motives and arguments were manifold the question – to join or not – was clear and unequivocal.

The recent referendum had a clear “yes” option in the “Remain” but the “no” option, “Leave,” was ambiguous. Wrapped up in the “Leave” was Ukip’s original goal of Britain leaving the EU, never a mainstream opinion in Britain until the referendum – and the stated goal of many Tories inter alia Boris Johnson who argued for his position by claiming Britain would secure a better deal by voting “Leave.”

Bumpy start… towards ashen Tory faces

Farage’s “out” and the “get a better deal” propagated by non-Ukipers gave the “Leave” campaign a bumpy start. Interviews with the Tory “Leavers” waving the “better deal” gave rise to the obvious question what would qualify for a “better deal” leading to unexciting answers.

With the “Take control” slogan things took a better turn for the “Leavers.” Although that also invited convoluted discourse – control of what and what would this new era of British control imply – this slogan could be connected to all relevant issues, be it immigrants or the NHS.

Now, the various sentiments awoken earlier by the fringe Ukip could easily be merged into mainstream Tory speak, useful not only to unruly Tory backbenchers but to leading Tories like Johnson and Gove.

As the voting stations closed June 23 Farage still seemed to believe his long-time apparently so ludicrous goal of pulling Britain out of the EU was lost; seven hours later he was a triumphant if stunned winner.

Contrast Farage’s celebratory appearance with the funeral demeanour of Johnson and Gove when they finally made a public appearance late Friday morning. Their ashen faces indicated they realised they would now need a plan, which they didn’t have. Demagogy and burning ambitions are two sentiments notoriously difficult to harness – a few days later their political fortunes had turned but that is another story.

Farage, leading a fringe party, didn’t feel obliged to have a plan. He had wanted a Brexit, getting it was all he needed to claim victory and he could resign (though given his career of resignations it’s a different matter if he really is leaving politics).

The Ukip xenophobia: from extreme to mainstream

Damian Green’s epitaph of Farage building his political career by encouraging destructive ideas sums up one view of Farage’s political contribution. Farage may fade out of UK politics but his message lingers on among those who took note of his message as they had never before. Not because his message was better or different than it has been for decades but because established and leading politicians adopted and legitimised his stance.

By adopting Farage’s stance on the EU, Brexit supporters like Gove and Johnson, not to forget Andrea Leadsom, also propagated the other part of the Ukip’s political bill, the xenophobia with a whiff of racism. Here, the “Remain” stance of the Labour leadership, especially Jeremy Corbyn, was lamentably weak.

Leading Brexiters from the two big parties vehemently deny xenophobic intentions and undertones but that is too late: thanks to the Brexiters outside of Ukip these views have entered the political discourse. Again, what once was extreme is now mainstream.

The once so loony and laughable

To be exact, this legitimation hasn’t only happened in the last few months. For years, instead of rebutting the often hugely misleading statements from Ukip on immigration with facts and figures established mainstream politicians came to echo the Ukip view. Also, by not engaging the fact that concerns on immigration were the embodiment of simmering anger over political failures since the 1980s was lost.

Already in 2006 Cameron called Ukip “a bunch of … fruticakes and loonies and closet racists mostly.” Like Cameron, established politicians saw Ukip as a crazy fringe party: there was no need to argue with Ukip, no need to correct Ukip-ers’ misleading statements. In the media, largely sympathetic to Ukip’s views, the party was often ridiculed but almost in an endearing underdog way with Farage clowning on BBC’s Have I Got News For You.

With time, there was the seducing option for established politicians to use these sentiments for their own political advantage inter alia by blowing problems with immigration out of all proportions and blaming the immigration on EU rules.

The referendum “Leave” campaign showed that Ukip had by now shaped the immigration debate: further, its views were legitimised by Tory “Leavers” campaigning for a cause earlier only touted by Ukip with arguments earlier only used by Ukip. – This is the grin the parting Farage leaves in British politics.

Danish echoes

The Danish political environment is fundamentally different from the British one but similarly to what has been happening in Britain, xenophobic sentiments, tinged with racism permeated Danish politics in the years up to the elections in 2001. Ukip’s sister party Danish National Party emanating these ideas, jumped from a fringe position with 7% of votes to being the third largest party with 12% of votes and a decisive influence.

In the previous years DNP, founded in 1995 but an offspring of 1970s right-wing currents, had put pressure on the established parties, both the centre-right parties and the Social Democrats, leading many politicians to concede to and echo the DNP view instead of debating it. Buoyed by its 2001 results DNP came to shape Danish immigration policy and the political language: what could earlier not be said had been legitimised. With 21% of votes in the 2015 DNP is now the second largest party in Denmark after the Social Democrats.

Interestingly, in Denmark immigration hasn’t been blamed on EU but been a domestic bone of contention. In spite of sceptic EU-attitude there is no appetite in Denmark to leave the EU and hasn’t been for years. DNP, which used to be anti-EU has without fanfare abandoned its anti-EU stance.

There is however a Danish Brexit effect: opinion polls show increased support for Danish EU membership and less appetite for a Danish referendum on membership. Before the British referendum 40% of Danish voters wanted a referendum on Danish EU membership, 60% preferred to stay in the EU and 22% wanted to leave; now these numbers are respectively 32%, 70% and 18%.

Abdicating political responsibility

When David Cameron, under pressure from Ukip, promised a referendum he might have been lured by an easy game against “loony fruitcakes.” Following an albeit narrow win in the 2014 Scottish referendum and in the 2015 general elections he lost the EU referendum and together with that loss, xenophobia and worse has come to stay in British political debate.

The economist Joseph Schumpeter (1883-1950) claimed the welfare system would be in danger when the sense of entitlement to gain from it was greater than the will to contribute to it. Similarly, democracy is in danger when politicians take it too much for granted and can’t be bothered to argue with ideas that undermine it. After all, being in power means not only having power to take action but also to sway and influence opinion.

Cross-posted on A Fistful of Euros.

Follow me on Twitter for running updates.

Let them litigate

“Iceland’s selective default?” was the topic of a seminar in New York this week, organised by EMTA, the association of emerging markets investors. The measures taken by the Icelandic government and the Central Bank to reduce the offshore króna have placed the question mark in the question. Sadly, that question mark was not erased at the meeting but that doesn’t seem to worry the Icelandic government.

The concept selective default has been waved around recently in connection with the measures taken by the Icelandic government: at the strategic time, just before – what is or was to be – the last offshore króna auction, two foreign experts waved the “selective default” banner in Wall Street Journal and FT Alphaville (see my latest on this).

The two writers were present at the EMTA event in New York, James Glassman as the moderator, with Arturo Porzecanski on the panel together with Magnús Árni Skúlason, an Icelandic economist advising some of the funds holding the offshore króna and Lee Buchheit from Cleary, Gottlieb, advising the Icelandic government.*

Very much contrary to how the estates of the failed banks were dealt with last year (as I have repeatedly pointed out) – when nothing was finalised until the creditors had agreed to the measures – the Icelandic government, advised by Cleary, is engaging with offshore króna holders, to use an Icelandic expression, “with two ram’s horns,” meaning belligerently. Or as Buchheit said: let them litigate.

It is indeed a real possibility that the largest funds will litigate their way through this mess. The question is what that would entail for Iceland in terms of inter alia long-lasting and costly litigation, negative effect on credit ratings and possible delays in lifting capital controls, the goal of the whole exercise. In addition, several interesting points came up in the debate: the banks’ estate v offshore króna; recent restrictions on inflows; discrimination based on nationality – and was the recent auction really the last one?

Litigation: a real threat?

Icelandic authorities have deemed the auction successful because of good participation although CBI governor was more cautious. True, there were plenty of bids – but small ones. The large offshore króna holders didn’t participate or their offers weren’t accepted. Ergo, the bulk of the offshore króna is still inside capital controls. There is now litigation in the air, the largest offshore króna holders, all large international funds, have taken the first steps in that direction. The question is what the effect on Iceland and the Icelandic economy will be.

Buchheit said he wanted to puncture what the articles by Glasman and Porzecanski stated. He dismissed that the offshore króna holders had any claim on the Icelandic sovereign. Waving a dollar note, he stated that owning this note didn’t make him a creditor to the US; equally, owning a króna didn’t make the offshore króna holders a creditor to the Icelandic sovereign. – However, the large offshore króna holders aren’t waving króna bills but Treasury securities; around 2/3 of the offshore ISK319bn are Treasury securities which makes the situation slightly more convoluted.

Dismissing any comparison with Argentina, Buchheit did however neither directly counter the argument that the underlying assets are indeed Treasury securities nor give any tangible argument against the Argentina comparison except claiming it was not true. The funds could try litigating but neither Britain nor the Netherlands had found great sympathy for their cause, he said.

This must refer to the Icesave dispute, ruled on by the EFTA Court in January 2013 (link to the Judgement and my digest of the main points.) From the point of view of Iceland this seems a worryingly feeble argument since that dispute was, as far as I can see, fundamentally different from the issues at stake re the offshore króna (see below). Also, the argument that the offshore króna holders had bought their assets with a haircut inside capital controls seems beside the point; the point is that an owner of these securities can demand a payment on time and in full.

The testing point will be if courts – in Iceland and possibly elsewhere – will side with offshore króna holders or not. After all, Argentina decided to negotiate with those holding Argentinian sovereign bonds after a costly dispute lasting 15 years where Cleary Gottlieb was their main adviser (but not Buchheit until at the recent and final negotiations).

Cooperation last year, none this year

It now seems that the Icelandic strategy is to fix the offshore króna overhang with this last auction with remaining funds placed on locked low-interest accounts with the CBI, as the Treasury securities reach maturity, thus ignoring the possible legal risk. The next steps will then be towards lifting controls on the domestic economy, most importantly the pension funds. Only later will the locked accounts be revisited.

Magnús Árni Skúlason stressed that the funds he advised had come up with many proposals as to how to solve the issue. He pointed out that due to the very strong and booming Icelandic economy and sizeable foreign currency reserves it was difficult to argue for a haircut on grounds of a weak economy.

As I’ve repeatedly pointed out I find the difference in approach last year with the creditors of the failed banks and now with the offshore króna holders perplexing. In the latest IMF Article IV Consultation with Iceland, concluded on June 20, the IMF compares its 2014 recommendations with Authorities’ responses. On capital controls the IMF recommended in 2014 that the “updated liberalization strategy should be comprehensive, conditions based, and with an emphasis on a cooperative approach with appropriate incentives.”

As to the Authorities’ response the “updated liberalization strategy released in June 2015 takes a staged approach. The bank estates were resolved first, in a cooperative manner, which minimized legal and reputational risks and won credit rating upgrades. The authorities are now working to release offshore króna investments via an auction. Residents will be addressed thereafter (emphasis mine).

Minister of finance Bjarni Benediktsson has earlier emphasised the same as the IMF above, as did Buchheit at the EMTA meeting, that creditors have not challenged the measures last year in lifting capital controls on the banks’ estates. Due to the “cooperative manner” last year there were no legal challenges, which again raises the question why it’s suddenly not important to avoid the legal and reputational risk. So far, no clear answer.

Misconceptions on Icelandic “vindictiveness”

In his FT Alphaville guest blog Arturo Porzecanski criticised the Icelandic government for its measures on offshore króna, pointing out that the measures would place Iceland in selective default. He also strongly criticised recent law authorising the CBI to impose measures to discourage foreign inflows into Iceland.

Porzecanski embellished his points further at the EMTA meeting. According to him, the Icelandic government is, in his words, being “vindictive;” as if investors were responsible for the 2008 crisis, the government now wanted to “bleed investors” as it had tried last year with what he called a “departure tax” on creditors of the failed bank. However, he didn’t mention that the outcome an agreement with creditors (see my blog). To him this all smelled of punitive coercive action, just as in Greece and Argentina.

The tone in Iceland towards foreign investors has at times been harsh, mainly because of the politics at play, but Porzecanski’s description is to my mind out of proportions. After all, a 2010 report by an Icelandic Special Investigative Commission on the 2008 banking collapse, firmly and squarely placing the responsibility with Icelandic authorities, the CBI and politicians. And Icelandic bankers have been sentenced to imprisonment for criminal actions before the collapse of the banks.

The measures to temper inflows have long been expected: already in 2012 the CBI published a report on Prudential Rules Following Capital Controls, outlining what is needed to preserve financial stability once the capital controls have been lifted. Quoting IMF research one of the measures announced is restricting inflows, as indeed many countries have done over the past decades.

Porzecanski claims this is just done because the inflows were seen as a problem earlier, saying there is no justification for this measure. Well, he is right that the inflows were seen as a problem earlier, indeed the capital controls were put in place with the blessing of the IMF because of inflows, now the offshore króna overhang. As Porzecanski should be aware of and as emphasized in the 2012 report, IMF research underpins these measures, as do many economists. From the publication of the 2012 report it was clear that in due course these fairly traditional restrictions would be made use of.

Discriminating between foreigners and Icelanders?

A question from the audience at the EMTA event, on potential discrimination between Icelanders and foreigners, raised some interesting issues. The point was that Icelanders holding a króna would get a full króna whereas the offshore króna measures subjected foreign króna holders to getting only say 70 aurar (100 aurar = 1 króna). Buchheit’s point was that there was no discrimination involved. – Yet, the question still raises an interesting aspect.

The Emergency Law, passed on 6 October 2008 did differentiate between deposits held by individuals and entities domiciled in Iceland and abroad (which has partly shaped the definition of the offshore króna). This division was in fact a version of splitting the banks into a bad and good bank since roughly the foreign loans were put into the estates and Icelandic deposits into the new, living banks (it was slightly more complicated but this is the rough outline). – The Emergency Law has been contested in Icelandic courts and found to be in accordance with the constitution and Iceland’s international obligations.– These were extreme measures in extreme time taken by a sovereign defending its vital interests.

Eventual discrimination came up also in the Icesave case as the EFTA Surveillance Authority claimed in the EFTA Court, focusing on the use of the Icelandic Deposit Guarantee Fund, TIF. The question of discrimination was deflected in the Judgement due to the course of events in Iceland: the deposits had indeed been moved from the failed banks to the new banks but not reimbursed by the Icelandic TIF. Consequently, the Icelandic TIF didn’t need to reimburse foreign depositors, i.e. there was on discriminations involved and no breach of the relevant Directive. – Maybe it’s my lack of legal intricacies but I don’t quite see the relevance of the EFTA Court Icesave Ruling for the offshore króna problematic (as above, link to the Judgement and my digest of the main points.)

Is this really the last auction – and more confusion

In his introductory remarks Buchheit mentioned offhandedly that there are FX auctions all the time and this latest one was just another auction, in a series of 22 offshore króna auctions. Porzecanski asked if this meant this latest really was just another auction, would there be auctions following this announced last one but got no answer.

Porzecanski also pointed out that this last auction was indeed not a proper auction, more like bringing work of art to an auction house which then would set the price, i.e. no bidder on the other side.

During the question and answer session Skúlason mentioned that one concern of his was that part of the underlying assets was indeed Treasury bonds. Buchheit agreed there were some bonds, which would be paid in full and on time as Iceland had a stainless record in terms of fulfilling its sovereign obligations: it has never defaulted. – This statement seems to conflict with earlier statements – unless there is some tricky teleological interpretation behind the advice to the Icelandic government.

Last year, my main worry regarding the estates of the failed banks was if the government was ever going to have the political strength to agree on the necessary measures (mainly the haircut of the estates’ króna assets) and secondly that these measures would steer clear of legal risks. This year, the worry is that for some inexplicable reasons the cooperative method isn’t in vogue, in Iceland, possibly leading to legal risks and reputational damage so astutely avoided last year. Maybe I’m missing something but the discussions at the EMTA meeting didn’t inspire much confidence: “let them litigate” sounded decidedly belligerent compared to the cooperative approach last year.

*I had been invited to join the panel but ended up only listening via phone from London.

Follow me on Twitter for running updates.