Search Results

The Legatum Institute: the charity and its offshored sponsor

Special-interest billionaire-funded organisations have for years been a common feature in US politics but less prominent in the UK. The UK Legatum Institute, now influential in pro-Brexit government quarters, seems to fit the US formula. It played a curious role in an Icelandic dispute in 2016 with some US funds holding offshore króna. That story throws an unflattering light on Legatum’s research and exposes intriguing US connections. In a wider context it is a cause for concern that sponsors of British charities can hide behind the offshore veil.

In October 2016 the Icelandic government suddenly found itself the target of an international ad campaign. With a photo of Central Bank governor Már Guðmundsson the Icelandic Central Bank was accused of corruption. The government was said to follow “protectionist economic policies” discriminating against offshore króna investors, in reality four American funds. Not a word on the fact that the policy of the Icelandic government was formed in close cooperation with the International Monetary Fund.

The ads ran in international media like the Financial Times, WSJ and Danish media, in addition to Icelandic media. The ads were signed by “Iceland Watch,” run by Institute for Liberty, which claimed to be a think tank.

One of the ads cited “a research team in Britain” that claimed the action against the offshore króna investors cost each Icelander between $15,000 and $27,000 a year, causing the loss of 30,000 jobs, quite fantastical figures in the context of the Icelandic economy. These findings were taken from a report, Frozen Capital: a Case Study of Icelandic Distortions by Shanker A. Singham and A. Molly Kiniry at the Legatum Institute.

Now that Legatum’s staff is publishing Brexit reports and popping up as Brexit-advisers in Whitehall Legatum’s Icelandic report and the ties it shows throws an interesting light on the Institute’s operations.

Iceland Watch and “Dark Money”

Until the ads appeared, Institute of Liberty and its Iceland Watch had been wholly unknown in Iceland. Institute of Liberty was however a familiar name in US politics. In her book, Dark Money; The Hidden History of the Billionaires Behind the Rise of the Radical Right, the American journalist Jane Mayer recounts how billionaires like David, Charles and Bill Koch, Peter Singer and lately Richard Mercer, much strengthened by the 2010 Citizens United ruling, have poured money into politics for decades, inter alia advocating in favour of tobacco and petro-interests and against Barack Obama’s healthcare.

Part of the funds to fight Obamacare flowed into a tiny organisation called Institute for Liberty. In 2008 its budget had been $52,000. The following year, it got $1.5m from the DCI Group, a Washington PR company, used for “a five-state advertising blitz targeting Obama’s health-care plan;” $400,000 were channelled back to DCI Group for “consulting.” (Mayer, p.192)

DCI turned out to be instrumental in spreading funds to groups fighting Obamacare, some of which, according to Mayer, “appeared to be shell organizations fronting for DCI Group.” One of them was Institute for Liberty. As a recent Bloomberg story (with a link to Icelog) shows the DCI Group’s operations are essentially lobbying in disguise, greased by ample funds from opaque sources.

The “dark art” of the DCI Group and Legatum Institute

At the end of October 2016 the following ad ran in Icelandic and international media, under a photo of Central Bank governor Már Guðmundsson:

“Who is paying for public corruption and discriminating rules in Iceland? You do!

The decision taken by the Central Bank of Iceland to discriminate between investors so that only those of domestic origin can invest there has been criticised internationally.

According to a new study done by a research team in Britain the discriminatory policy of the Icelandic capital control hinders the creation of 30.000 new jobs and costs the nation between 5.000.000.000 and 9.000.000.000 US dollars in GDP annually.

This costs each Icelandic citizen between 15.000 and 27.000 US dollars annually.”

In the context of the Icelandic economy these figures are rather implausible. How could offshore króna controls hinder the creation of 30.000 jobs in an economy with close to full employment in a country of 332.000? The stated cost of $5bn to $9bn amounted at the time to 25 to 40% of Icelandic GDP. – In short, the figures were outrageously unintelligent.

The figures came from a Legatum report, Frozen Capital: a Case Study of Icelandic Distortions by Shanker Singham and Molly Kiniry, published in autumn 2016. At the same time, the Legatum Institute held a debate on Iceland and the capital controls (which by then had been lifted except for the offshore króna controls), Post-Brexit Briefing: Frozen Capital – A Case Study of Iceland. Judging from the recording, using Iceland as an example of harmful trade distortions was greatly undermined by the fact that the speakers, Singham and Iain Martin former editor of the Scotsman were rather uninformed on Iceland, in line with the report.*

My own inquiry at the time showed that the DCI Group orchestrated the Iceland Watch ad campaign in autumn 2016 on behalf of three of the four American funds that held Icelandic offshore króna – Autonomy Capital, Eaton Vance and Discovery Capital Management. My understanding was that DCI, on behalf of the funds, had turned to the Institute of Liberty, i.e. the initiative came from the DCI, just as it had used Institute of Liberty and other organisations in fighting Obamacare.

Legatum’s Brexit reports

The Legatum report on the Icelandic offshore króna was remarkably unenlightened but had, for obvious reasons, a rather limited effect.

A Legatum report in November last year on Brexit, The Brexit Inflection Point; the Pathway to Prosperity, by Singham, Radomir Tylecote and Victoria Hewson is a different matter, dealing not with a minor matter in a liliputian nation but the a vital issue for a rather bigger nation and 27 other European countries.

The November report was not the first Brexit report from Legatum but it caught much greater attention than the earlier ones because by November, the British media had become aware of Legatum’s role in Westminster. Some journalists who gave it a close reading were less than impressed. FT’s Martin Sandbu wrote of “Beware the global Britain con trick.” In the same paper, Martin Wolf wrote on “Six impossible notions about “Global Britain” referring to the White Queen in C.L. Lewis book Through the Looking Glass who claimed to believe six impossible things before breakfast. Singham published an answer to Wolf’s article on CapX and a shorter version in The Telegraph, £) but ignored other critics.

Earlier Brexit-related reports were Mutual Interests: How the UK and EU can resolve the Irish border issue after Brexit published in September 2017. The point that caught media attention was that the border issue could be solved by technology; a claim that proved short-lived. In April there was a report on A new UK/EU relationship in financial services – A bilateral regulatory partnership. Two reports papers in February dealt with the negotiations and trade, Brexit: World Trade Organisation Process and Negotiation of Free Trade Agreements and Brexit, Movement of Goods and the Supply Chain. In November 2016 a report dealt with the Cost of EEA Membership for UK Briefing.

All reports were written by Singham, mostly in cooperation with other Legatum staff. The general tone is the one of the same kind of impossibility that Martin Wolf pointed out.

Legatum’s “Brexiteering”

At the Legatum Institute its main Brexit expert, Shanker Singham has the titles Chair, Special Trade Commission and Director of Economic Policy and Prosperity Studies.

Singham has two LinkedIn profiles; one states he is managing director for Competitiveness and Enterprise Development Project at Babson Global, the other that he is the Director of Economic policy and prosperity studies at Legatum and the CEO and Chair of Competere Group, operating all over the world. There is little information on Competere but according to the Legatum website it is an “Enterprise City development company incubated at Babson College.”

On the latter LinkedIn profile Singham states that Competere was set up in 1997 but later rebranded and has “successfully engaged governments around the world who seek to harness the power of the market economy through a comprehensive pro-competitive regulatory framework. Our economic reform practice is based on the use of our econometric modelling to help (23) countries successfully realize their own reform efforts.”

In the summer of 2015, Singham incorporated Competere Limited with 1,000 GBP in the UK. A year later the company was in deficit of just over £17,000.

Together with a Washington lobby group, Transnational Strategy Group and EPPA Brussel, Competere has set up a Brexit “practice group.” TSG claims to be a “boutique international business and foreign policy consultancy focused exclusively on achieving real results for clients.” EPPA claims to be a consultancy for “creating a constructive dialogue with policy-makers” elaborated with a quote from FT’s Martin Wolf: “We need a balance between markets and governments.” EPPA does not seem to flag the cooperation with TSG and Competere on its website (at least not within easy sight).

Singham, who has a dual UK US citizenship, worked at Squire Sanders, a US law firm from 1995 to 2013. Since April last year Michael Cohen, president Donald Trump’s personal lawyer has had a strategic alliance with Squire Sanders, now Squire Patton Bogs. Cohen is one of many in Trump’s inner circle with alleged ties to Russia and Russia’s president Vladimir Putin.

Singham’s co-author on the Brexit report in November, Radomir Tylecote, was active on the Vote Leave campaign before the 2016 referendum as was Victoria Hewson, the third author of the report.

Molly Kiniry, Singham’s co-author on the Icelandic report and other Legatum publications, is also listed as a consultant with Competere since 2016, earlier at Babson Global. She writes regularly for Daily Telegraph, where two of her recent columns dealt with “The virtue-signalling British Politicians snubbing Trump are embarrassing themselves” and “Americans are sick of sending money to other countries for no discernible benefit.” – The connection with Daily Telegraph is interesting given that the paper is owned by the Barclay brothers, two Brexiters with their wealth firmly offshore.

Former Chief Executive of the Vote Leave campaign Matthew Elliott, now a frequent voice in the British media, is a Legatum senior fellow. Georgiana Bristol, Legatum’s Corporate Membership Director, ran fundraising for Vote Leave. Two well-known names from UK politics have recently joined the Institute as Fellows: the fervent Brexiter ex-MP for Labour Gisela Stuart and Sir Oliver Letwin and MP. He voted remain, was briefly in charge of Brexit after the 2016 referendum before being replaced by David Davis by Theresa May and has been seen as a Tory intellectual close to libertarian ideas.

An ex-Legatum employee is already a Whitehall Brexit-insider: Crawford Falconer, who was on Singham’s trade commission at the Legatum Institute, is working as a Brexit negotiator under International Trade Secretary Liam Fox.

Legatum’s CEO Baroness Stroud has in the past made some unsuccessful attempts to be chosen as a Conservative Party candidate. She set up the Centre for Social Justice in 2004 with Ian Duncan Smith for whom she acted as a specialist adviser 2010 to 2015 at the Department for Work and Pensions. Stephen Brien, who leads Centre for Metrics at the Legatum is on the board of CSJ and was also Duncan Smith’s adviser, 2011 to 2013. Legatum and CSJ have had some collaboration.

From corruption to Brexit

In 2015 the Legatum Institute organised some events on corruption chaired by Anne Applebaum, i.a. one where she interviewed Sarah Chayes on her book Thieves of State: Why Corruption Threatens Global Security. It was at that time I first noticed Legatum. I welcomed Legatum’s focus and the clout and eminent experience that Anne Applebaum brought to the Institute as its director of Transitions Forum 2011 to 2015, focusing on new threats to democracy.

Judging from Legatum’s website the Transitions Forum no longer exists. Applebaum is now Professor in Practice at LSE’s Institute of Global Affairs where she leads Arena, a programme on the challenges of disinformation.

Legatum’s expanding role in Westminster has drawn media attention. A whole-page FT article in December 2017 on “Legatum: the think tank at intellectual heart of “hard” Brexit” claims the focus of Legatum shifted in autumn of 2016 when Baroness Stroud became a director and a trustee.

Former employees, said to be worried about the direction taken by the Baroness talked of purges. According to them, the organisation seemed to use its influence in Westminster “to push for a libertarian and socially conservative agenda that goes beyond its educational remit as a charity emphasising “prosperity and human flourishing”.” The question posed was if Legatum’s activities were compatible with its status as a charity.

FT mentions that Brexit minister David Davis has taken fees from Legatum. That was however in 2009 and 2010, according to They Work For You: £5000 for a speech and, interestingly, unspecified travel expenses to attend a conference at the Milken Institute that attracts those with libertarian leaning. According to information on They Work for You neither Michael Gove, Boris Johnson nor Liam Fox have accepted funds from Legatum. Davis gave however a talk at a Legatum Brexit event in January 2017, Gove was a guest speaker at the Legatum’s summer party in 2016 (according to Legatum’s 2016 annual accounts); neither seems to have been paid for their input according to the They Work For You data.

In late November Daily Mail published an article on Legatum’s political connections, ‘Putin’s Link to Boris and Gove’s Brexit Coup’. According to the paper, Singham had helped two Cabinet members, Boris Johnson and Michael Gove, to pen a letter to Prime Minister Theresa May. In the letter, not meant for publication, the duo called on May to put pressure on Chancellor Philip Hammond to prepare for “hard” Brexit, to use Brexit to scrap EU rules and regulations and to appoint a new “Brexit Tsar.” No Tsar has officially been appointed but the tabloid maintains that Singham effectively has that role.

Daily Mail pointed out that Legatum’s founder Christopher Chandler and his brother Richard got rich in Russia following the collapse of the Soviet Union. The tabloid tells the story of the brothers taking part in a boardroom coup in Gazprom in 2000, installing Alexey Miller, close ally of Vladimir Putin from their St Petersburg years. This enabled Putin getting a share in Gazprom’s profit.

Chandler and the Legatum Institute deny all allegations of Russian ties and also denied allegations made by The Sunday Times and Sunday Mail in early December regarding its status as a charity.

Legatum, on- and offshore

Legatum Group (legatum.com) is based in Dubai where it was set up in 2006 by Christopher Chandler. It describes him as former President of Sovereign Asset Management he set up in 1986 with no mention of his earlier Russian activities. Its website lists a whole raft of philanthropic organisations under its umbrella, the Legatum Institute being one of them.

The Legatum Institute’s own website is somewhat vague on the Institute’s funding. Under the heading “How we are funded” there is a list of four other philanthropic enterprises, funded by the Legatum Foundation (legatum.org), also listed under Legatum.com, but the link attached leads only to a website with the four enterprises.

There are two relevant Legatum entities listed with Companies House, The Legatum Institute Foundation, which is the registered limited company operating in London and the Legatum Institute, a fund registered in the Cayman Islands.

The Foundation is registered with the Charity Commission. Out of the £4.4m of its total income in 2016, £3.9m came from Legatum Foundation Limited, according to the Legatum Institute Foundation’s 2016 full accounts at Companies House. That year the Foundation received £437K from other sponsors than its “lead sponsor, Legatum Foundation ltd … demonstrating its continued journey towards financial independence.”

The accounts do not hold any information on the real sponsor, Legatum Foundation Limited nor is it registered in the UK, judging from Companies House. The Legatum Institute Foundation has confirmed it will fund the Institute until end of 2019. As can be seen from the above figures there is still some funding to cover to match the Foundation’s funding.

According to the FT the charity has 40 donors in addition to its lead sponsors, but interestingly the charity is unwilling to disclose who these donors are – a peculiar situation for a charity.

The Legatum Institute fund was registered in the Cayman Islands in 2008. Its objective is “Philanthropic development.” The three present directors, Alan McCormick, Mark Stoleson and Philip Vassiliou, are all registered at Legatum Group’s address in Dubai. According to the 2016 full accounts of the Cayman fund at Companies House, its assets in 2016 were $8,9m, $24m in 2015.**

Christopher Chandler and Mark Stoleson have recently obtained EU passports through the widely criticised Maltese passport-for-investment scheme.

Legatum fits the “Dark Money” format of billionaire-funded partisan US think tanks

Intriguingly, Legatum’s founder and main sponsor fits the model of the American billionaires who for decades have been funding make-believe institutions to influence politics and confuse public debate. Christopher Chandler keeps firmly out of the limelight and his name off documents: people working from him are directors of his companies. The array of Legatum entities, on- and offshore, is rather bewildering and runs contrary to the transparency that charities could be expected to adhere to.

There are indications that some of those fighting for Brexit are inspired by Russian and American ideas of how to gain power by dividing and ruling, by sowing disharmony. The Kremlin propaganda machine is inspired by Vladimir Putin’s longtime political technologist Vladimir Surkov and his ideas of “non-linear wars” and other means of profiting from confusion and shifting alliances.

Paul Manafort, Trump’s campaign manager, has been indicted with conspiracy against the US, tax evasion and money laundering, as part of the investigations into Russian collusion in the US presidential elections. The Ukrainian journalist and politician Serhiy Leshchenko has explained how Manafort operated in Ukraine by putting into practice the politics of division and social polarisation.

There is of course nothing wrong with airing one’s views. But airing it on false premises is insidious and undermines public debate. And false or biased information is one way of playing the politics of division.

As Jane Mayer describes so well in her book, key strategy of billionaires is to fund organisations that produce something that looks like “research” but is indeed propaganda. This has been an effective strategy in fighting for the interests of the tobacco industry and the petro-industry, not to mention Obamacare. The damage is done when the media embraces this research as equally valid to thoroughly researched material. The danger is media unwilling to or uninterested in distinguishing between the propaganda and carefully researched studies.

Another aspect of the propaganda-driven organisations is the opacity of their sponsors, normally offshored and out of sight. The offshoring should indeed be a sure sign of warning.

These propaganda organisations have so far not been prominent in the UK. Legatum Institute, funded by Christopher Chandler, seems to fit the US model of a propaganda-driven “think tank.” Thus, their reports should be read with that in mind. The two reports, on Iceland and Brexit, certainly seem a poor addition to an enlightened discourse on these two topics.

* I pointed these figures out to a Legatum employee who forwarded them to Singham. His response was that the data was “based on the application of our ACMD productivity simulator (for more information, please see the attached link).” He agreed I made a valid points regarding the employment effects and Iceland’s small size. Consequently, they would “probably … not focus on employment effects too much in the deeper analysis. While capital controls are generally distortionary from the perspective of an open and liberalized trading environment, the precise manner of their amendment or repeal also can have distortionary effects. The data is picking up the implicit national treatment violation as a function of the key variables on property rights and foreign investment in our simulator.” – The analysis on the website is still as it originally was, with the implausible figures.

**According to Companies House records 8 March 2018, the Cayman fund is now in administration.

Follow me on Twitter for running updates.

Paradise Papers and the onshore heart of the offshore industry

The Paradise Papers emphasises, yet again, that the damaging effect of offshore is much more pervasive that robbing countries of tax. Offshore creates a two-tier business environment, hiding ownership and in general throwing an opaque veil over the offshored part, thus undermining competition, regulation and ultimately the rule of law. The offshore alchemists also need the rule of law – the heart of the offshore industry is firmly onshore in countries with the stability provided by rule of law. As juicy as it is to read about famous individuals benefitting from insane offshore projects, the offshore enablers are onshore in fancy metropolitan offices, the heart of the offshore industry. Shaming, scrutinising and exposing the enablers needs to be part of anti-offshoring policies.

Yet again, a major leak is deepening our understanding of how wealthy individuals and companies make use of the offshore universe. The Panama Papers provided insight into wealth management of private individuals. Apart from further insight into the same, the Paradise Papers show how big companies like Apple and Nike use the power of wealth and offshore craft to negotiate tax reductions with governments and authorities.

In addition, the leaks underline that offshore isn’t just about tax. It’s about secrecy and opacity; the concept of secrecy jurisdiction as the Tax Justice Network defines it gives a much clearer understanding of the nature of offshore. And secrecy undermines markets, governments and the rule of law.

Intriguing as it is to think of warm and exotic places like the Bahamas or Seychelles, places lacking any infrastructure needed to oversee the oceans of money floating through them, at least on paper, the heart of the offshore industry is firmly onshore. It is in cities like London and countries like Switzerland and the US where the best paid offshore experts and enablers live and work.

Iceland – (possibly) the most offshorised country in the world

Through serendipity and coincidence, the first thing I started digging into after the collapse of the three main Icelandic banks in 2008 was their offshore operations, mostly in Luxembourg. A whole new dimension of the Icelandic banks and businesses opened up when I discovered how to search the Luxembourg Gazette for Icelandic links.

Apart from the well-known Icelandic tycoons operating abroad I found dozens of Luxembourg companies connected to people I had never heard of. When I contacted some of them it turned out they were mainly owners of small companies. One of them had sold a small fishing boat for around £15.000.

In all of the cases I looked into, the banks had suggested the client should offshorise, set up a company in Luxembourg and move their funds abroad – a good example of the role of the enablers. If the client both paid tax and the offshore fees offshoring didn’t make much financial sense; it was more lucrative to hide this from the tax and then for example have a foreign credit card to make use of the funds in Iceland, out of sight from the Icelandic Inland Revenue (which now keeps an eye on the use of foreign credit cards by Icelanders in Iceland).

What made the Icelandic offshoring so interesting was its pervasiveness: in no other country I know of did the banks set the asset bar so low, i.e. they advised offshoring as little as £10.000-15.000. After the collapse, some of these owners discovered how difficult and costly it was to revert the offshorisation and move their funds again to Iceland.

A 2016 report (in Icelandic) on Icelandic offshore assets, published in the aftermath of the Panama Papers, estimates that Icelandic assets in low-tax regimes 2015 amounted to ISK580bn, just over 25% of GDP that year. A staggering amount, four times the Danish figure; it explains to some degree why so many Icelandic names were found in the Panama Papers.

Offshore ultimately undermines the rule of law

In a small country like Iceland it is easy to see how offshore creates a two-tier business environment where only the onshore is in sight but the offshore part hidden from authorities and the public.

The operations of banks and businesses, the main players in the boom up to the collapse of the banks in October 2008, were thoroughly exposed in the 2010 report of the independent Special Investigation Commission, SIC. One of its findings was that fourteen foreign entities with unidentified owners owned more than 10% in 410 Icelandic companies (see Vol. 9 p. 79-83; in Icelandic).

Hidden ownership can be (ab)used in various ways. With ownership hidden abroad, large shareholders can control companies but avoid take-over regulations. Small investors who might steer clear of investing in companies of certain owners or under majority control, will be misled if some shareholders hide ownership offshore.

The latest example of intriguing interplay of offshore and ownership is the story of Alisher Usmanov in the Paradise Papers and his allegedly hidden ownership of Everton, in addition to his 30% of Arsenal; possibly a breach of Premier League rules.

The offshorised life: offshorised watch, offshorised children

Apart from the insight into the offshore craft, how offshore experts organise the offshore affairs of wealthy individuals and international companies, the story of the self-acclaimed “tax alchemist” James O’Toole is shows how offshore is now a life style.

O’Toole is a British lawyer, an offshore enabler. He runs a company called Ashton Court Chambers and has himself offshored his life down to assets such as his £25.000 Rolex. Not a major financial asset though slightly more expensive than an Icelandic fishing boat but valuable enough to be offshorised. To satisfy British tax authorities O’Toole surmised it would be enough to pay his own offshore watch-holding company £50 a month to make it look like a wholly legitimate set-up.

Another example of Ashton Court tax alchemy is the “Educational Purpose Trust,” set up in Mauritius in 2013. It’s not for the benefit of school children on the island but for children of some wealthy individuals, clients of Ashton Court attending British private schools. Once their application was accepted (no examples of the contrary) the applicants were asked to make a “charitable donation” to EPT, exactly equivalent to the school fees/grant, in addition to a donation of £1000 – not for administration but for an “orphan child.”

Legal or not? Not the most pertinent question

Much of offshore activities is entirely legal. But the distinction between legal and illegal is far from always visible to the naked eye.

Statements issued by lawyers working for those whose names have come up in the Panama Papers and now in the Paradise Papers, claiming there is nothing illegal in the exposed schemes are rarely worth the paper they are printed on. These statements almost never come with any tangible evidence. The statements mainly show that those offshorised are likely to be well lawyered.

Further, the question of legality isn’t even the most important question. The effect of offshore is to hide and that in itself is the damaging effect. The corroding influence is the two-tier business environment, the visible onshore, the invisible offshore.

The offshore effect on poor … and rich countries

In exposing hidden offshore wealth, the focus is often on how poor countries lose substantial amount of their wealth abroad, often due to the vicious combination of corruption and offshorisation.

Offshoring corrupt funds exacerbate the underlying corruption. In order to make full use of corrupt money at home it is crucial that it can’t be seen who really owns the funds. That is done by offshoring them: by sending the money out of the country and back ownership and origin of the funds become invisible. Creating this invisibility is largely the work of offshore alchemists – bankers, lawyers and accountants – in London and other Western countries.

However, I would argue that the corrosive effect of offshored wealth is no less damaging to the wealthy developed countries but measuring and demonstrating this effect is more difficult.

The two-tier business environment is one thing: it undermines competition and regulation by exempting part of the business community from rules and regulation. Further, offshore funds make it easier for big business and wealthy individuals to influence politics, again by creating loops to send money out and get them back, for example when paying lobbyists, funding think tanks and in other ways influencing the political debate and legislation.

Ultimately, if flow of funds from offshore into these activities is pervasive enough, it could be argued that the rule of law, the fundament and pride of Western democracies, is dangerously undermined. What the offshore enablers don’t seem to understand is that undermining the rule of law is also harmful to their business: after all, the reason why it’s better to run an offshore business from London rather than Kinshasa is exactly the rule of law. Rule of law provides stability in addition to respectability.

That is why the heart of the offshore is onshore. Without the onshore heart, where offshore experts at the Big Four – PwC, EY, Deloitte and KPMG – and others in similar position feel at ease, the offshore business and its enablers would be a lot less potent. Actions to throw open the offshore universe, the secrecy jurisdictions, need to be directed at the onshore heart of the offshore industry.

The onshore presence, found at fancy addresses in gleaming offices in London, New York and elsewhere gives the offshore business legitimacy and gravity. Gravity the offshore enablers use to influence the legislative process, politicians and regulators in Western democracies in order to nourish the socially harmful industry of offshoring.

Shared by Tax Justice Network blog.

Follow me on Twitter for running updates.

Capital controls abolished – offer to offshore króna holders

As Már Guðmundsson governor of the Icelandic Central Bank, CBI underlined at a press conference today ordinary Icelanders have not felt the capital controls for a long time. Today, the controls are lifted for not only individuals but also for companies and the pension funds. Earlier limits have been lifted – de facto the capital controls are coming to an end in Iceland, more than eight years after they were put in place end of November 2008.

What remains in place is the following, according to the CBI press release:

i) derivatives trading for purposes other than hedging; ii) foreign exchange transactions carried out between residents and non-residents without the intermediation of a financial undertaking; and iii) in certain instances, foreign-denominated lending by residents to non-residents. It is necessary to continue to restrict such transactions in order to prevent carry trade on the basis of investments not subject to special reserve requirements pursuant to Temporary Provision III of the Foreign Exchange Act and the Rules on Special Reserve Requirements on New Foreign Currency Inflows, no. 490/2016. Guidelines explaining the above-mentioned restrictions will be issued to accompany the Rules.

The measures announced today were mostly as could be expected. However, the unknown variable was what offshore króna holders would be offered. Last summer they were offered a rate of ISK190 a euro; the onshore rate was ca. ISK140 at the time. The four large funds holding most of the remaining offshore króna – Loomis Sayles, Autonomy, Eaton Vance and Discovery Capital Management – refused that offer and have since been locked into low interest rates with an uncertain date of exit.

Now the offer is quite a bit more attractive: ISK137.50 a euro; the onshore rate is today ISK115.41. Last year, the offshore króna holders were offering ISK160 a euro, quite a bit better had the government been willing to accept it last year.

The CBI has lowered its bar, presumably because getting rid of the offshore króna holdings is seen as a bonus for Iceland. The sums captured inside the capital controls now amount to ISK195bn, less than 10% of GDP. Settling this last important part of trapped offshore króna means that Iceland can now take a step out of the shadow of the 2008 banking collapse – a chapter is coming to an end.

Former prime minister and former leader of the Progressive party Sigmundur Davíð Gunnlaugsson, forced to resign because of his offshore holdings exposed in the Panama papers, wrote today on Facebook that now the vulture funds were being rewarded; the funds had known they could crush the Icelandic government and that’s what they have now done. Others will beg to differ.

According to governor Guðmundsson the amount of offshore króna exiting at the new offer is just under ISK90bn. As far as I’m aware three of the four large funds have agreed to the present offer, which remains in place for the coming two weeks. One fund is considering its options, which must include testing the legality of earlier measures, a route the funds had already embarked on.

In total the four funds hold ISK120bn, further ISK12bn are holdings in shares, which are not being sold (thus nothing volatile there) and ISK60bn are deposits owned by various investors (some of whom might well have forgotten about their holdings or who are for some reason unaware of being the lucky owners of some Icelandic króna).

This means that although ISK90bn is less than half of the remaining offshore króna it’s roughly 3/4 of the offshore króna that could potentially move (though the funds do indeed want to keep their Icelandic relatively high-interest króna assets but that’s another saga).

What now remains in place is hindrance on inflows – as I’ve said earlier some would call it another form of capital controls but I side with the CBI that already in 2012 announced the conditions after capital controls would not be like before November 2008. Iceland isn’t interested in being the destination of money flows looking for lucrative interest rates. Consequently, prudent measures are in place since last summer.

Benedikt Jóhannesson minister of finance called today “a day of gladness.” Given that the controls had already been eased it’s unlikely the Icelandic króna will move much tomorrow or the coming days. The pension funds have good reasons to be vary of moving abroad. Though foreign investments would be wise as means of hedging foreign markets of low interest rates and high asset prices are not inviting.

Iceland is booming – the economy grew by 7.2%(!) of GDP last year. No exaggeration that there are good times in Iceland but good times aren’t necessarily easy times in a small economy with its own currency. With capital controls out of the way Iceland there is one thing less to worry about, the rating agencies will see this as a favourable move that might soon be expressed in more favourable ratings, eventually meaning lower interest rates in Iceland – so as to end on an optimistic note.

PS Why was the government keen to act now re offshore króna holders? Well, first for the entirely obvious reasons that Iceland is doing very well with large foreign currency reserves (not entirely trivial to invest them sensibly) and consequently it’s difficult to claim that economic hardship bars solution. In addition, as the minister of finance mentioned today: the rating agencies have indicated that the rating might move up, with the benefits such as lower interest rates when the sovereign borrows, spilling over into lower interest rates in Iceland. Last, it seems that the International Monetary Fund, very patient so far, was starting to air its worries: Iceland couldn’t keep boxing in the offshore króna holders indefinitely.

From top prime minister Bjarni Benediktsson, minister of finance Benedikt Johannesson (the two ministers are closely related, both from one of the most prominent business families in Iceland) and Már Guðmundsson governor of the CBI. Screenshots from the press conference today – notice the painting behind the two ministers: by Jóhannes Kjarval (1882-1972) the most iconic Icelandic artist, whose favourite motive was Icelandic landscape, most notable the lava landscape like here.

Follow me on Twitter for running updates.

Offshore króna owners allowed to seek independent estimates – inflows have stopped

An application with the Reykjavík District Court for independent assessment of the Icelandic economy, launched by two of the funds holding the majority of the Icelandic offshore króna, has been met by the Court. Originally, the funds had eleven requests; the Court granted three of them according the Icelandic daily DV.

The two funds claim the measures taken against the offshore króna holders this summer – effectively forcing them out at a great discount or freezing the funds at below-inflation interest rates – are harmful measures, utterly unnecessary in the booming Icelandic economy. They now want an independent assessment of the economy, in order to show that the Icelandic government could well afford more generous terms.

According to a recent decision by the EFTA Surveillance Authority the offhore króna measures were within the remit of the Icelandic government and did not break any EEA rules.

The measures no doubt had a sobering effect on foreign visitors but it the use of a new tool to temper inflows, announced in June this year that has had an effect: according to new figures released by the Central Bank, inflows into Icelandic sovereign bonds have completely stopped since June when the measures were put in place.

There had been some concern that the large inflows might jeopardise Icelandic financial stability as indeed it did in 2008 when capital controls were put in place exactly because of these inflows. Governor of Central Bank Már Guðmundsson said earlier this year that the renewed inflows, which the Bank would monitor, were a sign of trust in the Icelandic economy. Well, no worries – the measures in June stopped the inflows.

For earlier Icelog on the offshore króna issues please search the website.

Update: this piece has been updated as the earlier report re the effect on inflows was incorrect.

Follow me on Twitter for running updates.

ESA finds Iceland in compliance re offshore króna measures

The EFTA Surveillance Authority, ESA, has now closed two complaints re treatment of offshore króna assets by Icelandic authority: ESA finds the Icelandic laws in compliance with the EEA Agreement (see ESA press release here, the full decision here). The disputed laws were part of measures taken in order to remove capital controls in Iceland.

I have earlier written extensively about the offshore króna issue, also the rather bizarre action taken by the so-called Iceland Watch against the Central Bank of Iceland, which rubbed Icelanders, even those sympathetic to the point of view taken by the offshore króna holders, completely the wrong way. The sound points, which can be made by the offshore króna holders, were missed or ignored and instead the Iceland Watch action was shrill and shallow, based on spurious facts.

In general EEA states are permitted, under the EEA Agreement, to take protective measures when a states is experiencing difficulties as regards its balance of payments. As spelled out in the press release the states, in such situations, “are allowed to implement a national economic and monetary policy aimed at overcoming economic difficulties, as long as the criteria for these protective measures are met.”

As Frank J. Büchel, the ESA College member responsible for financial markets sums it up: “Iceland’s treatment of offshore króna assets is a protective measure within the meaning of the EEA Agreement. The overall objective of the Icelandic law is to create a foundation for unrestricted cross-border trade with Icelandic krónur, which will eventually allow Iceland to again participate fully in the free movement of capital.”

The funds in question, Eaton Vance and Autonomy, are testing their case in an Icelandic court.

Follow me on Twitter for running updates.

Iceland – lessons from an offshored country

Iceland is, in my opinion, the most offshorised economy in the world, from the point of view of how pervasive it was. The banks diligently sold offshore solutions as an everyman product. I talked about this topic as a Tax Justice Network workshop in spring. This was also the topic of an interview Naomi Fowler from the TJN recently did with me.

After the collapse of the Icelandic banks in October 2008 my attention turned to the role of offshorisation in Iceland. The banks operated in London, the Channel Islands and most important of all, in Luxembourg.

The widespread offshorisation, its effect and general lessons of offshorisation in Iceland was the topic of the interview Naomi Fowler did with me for Tax Justice Network recently, see here.

After my talk at the TJN spring workshop I wrote an article on the TJN see here.

The general lesson is: offshore creates an onshore shelter from tax, rules and regulation and thus creates a two tier society where tax, rules and regulation becomes optional for those offshored while living onshore, wether it’s in Iceland, the UK, US or elsewhere…

Follow me on Twitter for running updates.

Offshore króna holders with interesting friends

Holders of Icelandic offshore króna holders seem to have gained some intriguing friends. A so-called think tank, Institute for Liberty with the slogan “Defending America’s Right To Be Free” has suddenly found the urge to set up a project called “Iceland Watch” with its own website, specifically to follow, it seems, how Icelandic authorities deal with offshore króna holders (inter alia linking to some of my blogs).

The focus of interest, according to the Institute, is the following:

“The Institute for Liberty has followed Iceland’s path to recovery since the 2008 collapse and has developed an increased concern over recent protectionist economic policies like the discriminatory practices against offshore króna investors.

“In creating Iceland Watch, we aim to keep the public apprised of any anti-democratic and anti-free trade policies put into place by the Althingi, Iceland’s parliament, which could threaten the property rights of offshore investors in Iceland’s króna.

“Holders of Iceland’s offshore krona include several American investors, which serve a variety of retail investors like retirees with 401k plans and institutional investors such as corporate and public retirement plans, foundations, and endowments.

“Despite investors’ willingness to support Iceland during its time of transition and several distinct offers to negotiate good faith solutions, the Icelandic government refuses to offer anything other than a clear take-it-or-leave-it scenario. The discrimination against foreign investors is disturbing and could affect millions of American holders of 401k and retirement accounts.

“When Iceland’s parliament, the Althingi, convenes its Summer Special Session on August 15, its actions will indicate whether the island nation will reintegrate itself into international free markets or further its isolation by instating new costly, misguided policies that chill investment and economic growth.”

The Institute’s website indicates it’s also interested in Puerto Rico’s debt, another place where American investment funds struggle to get repaid. More intriguingly, the Institute has also fought Obamacare and other typically far-right interests.

Indeed, the Institute is part of ad hoc networks of “think tanks,” non-profit organisations and ,,grassroots” organisations funded by far-right American billionaires such as David and Charles Koch and the hedge fund owner Paul Singer, who for years fought the Argentinian government, now a settled issue.

The Institute is mentioned in Jane Mayer’s insightful and well-documented analysis of the money powers on the right-wing of the Republican party, far more right-wing than the mainstream Grand Old Party is. Powers, that for a few decades have pumped money into setting up phoney “grassroots” organisations in support of the tobacco industry, against environmental issues and lately, Obamacare. Mayer’s book, Dark Money; The Hidden History of the Billionaires Behind the Rise of the Radical Right, came out in spring, an essential read to understand the undercurrents in US politics the last decades and the issues behind political funding, now open to anonymous donations, and the Citizens United ruling in 2010.

According to Mayer, Institute for Liberty got lucky with funding, yet another node in the efforts to fight Obamacare; in 2009 it received $1.5m:

Four hundred thousand dollars of these funds were channeled back to DCI Group (Washington PR company, instrumental according to Mayer in fighting Obamacare) for “consulting.” The previous year, the Institute for Liberty’s entire budget had been $52,000. Suddenly it was so awash with cash that the group’s president, Andrew Langer, told the The Washington Post,‘ “This year has been really serendipitous for us.” He said a donor, whom he declined to name, had earmarked the funds for a five-state advertising blitz targeting Obama’s health-care plan. (Mayer, p.192).

As I’ve pointed out earlier, there have been some articles popping up here and there – op-ed in WSJ, guest blog on FT Alphaville and the most recent on The Street, “Iceland Should Learn From Argentina’s Bad Example” by Aldo Abraham, an Argentinian academic.

No need to point out that of course all of the media rumbling is orchestrated, driven as it is by non-journalistic input; as seen from Mayer’s book the DCI Group has links to the Institute. Everyone fights their turf as best they can, the links to the knights of dark money is rather unsettling but “à chacun son goût.” It is intriguing to see the cause of Icelandic offshore króna holders as part of this picture: not necessarily surprising but yes, intriguing.

The Princeton economist Angus Deaton, summarises masterly in his powerfully argued “The Great Escape” that the worrying trend in US politics is the tendency of interest groups to buy influence in Washington.

As spelled out in earlier blogs Argentina is potentially a worrying example for Iceland: it fought creditors and then settled after a decade of costly legal wrangling, beneficial for the lawyers involved and corrupt powers but deeply deeply harmful for Argentina. In Iceland, voices similar to those Argentinian politicians who fought the Argentinian debtors can be heard. Elections are coming up in October, politicians will hardly strife to be on the side of foreign creditors although successful plan last year re the estates of the failed banks, based on agreement with creditors, is a positive argument for co-operation with creditors.

Views vary: some claim Iceland’s cause is wholly different from Argentina. However, although Iceland has graduated from the earlier IMF program the Fund is still closely connected to Iceland; it’s difficult to imagine that the Fund’s views will be ignored. Happily, Iceland is blossoming and, according to the latest IMF report, has more than gained what it lost on the crisis, i.e. it’s difficult to argue for any emergency actions. In the end, Iceland will have to decide on the best course to follow so as to adhere to the rule of law and further prosperity.

Follow me on Twitter for running updates.

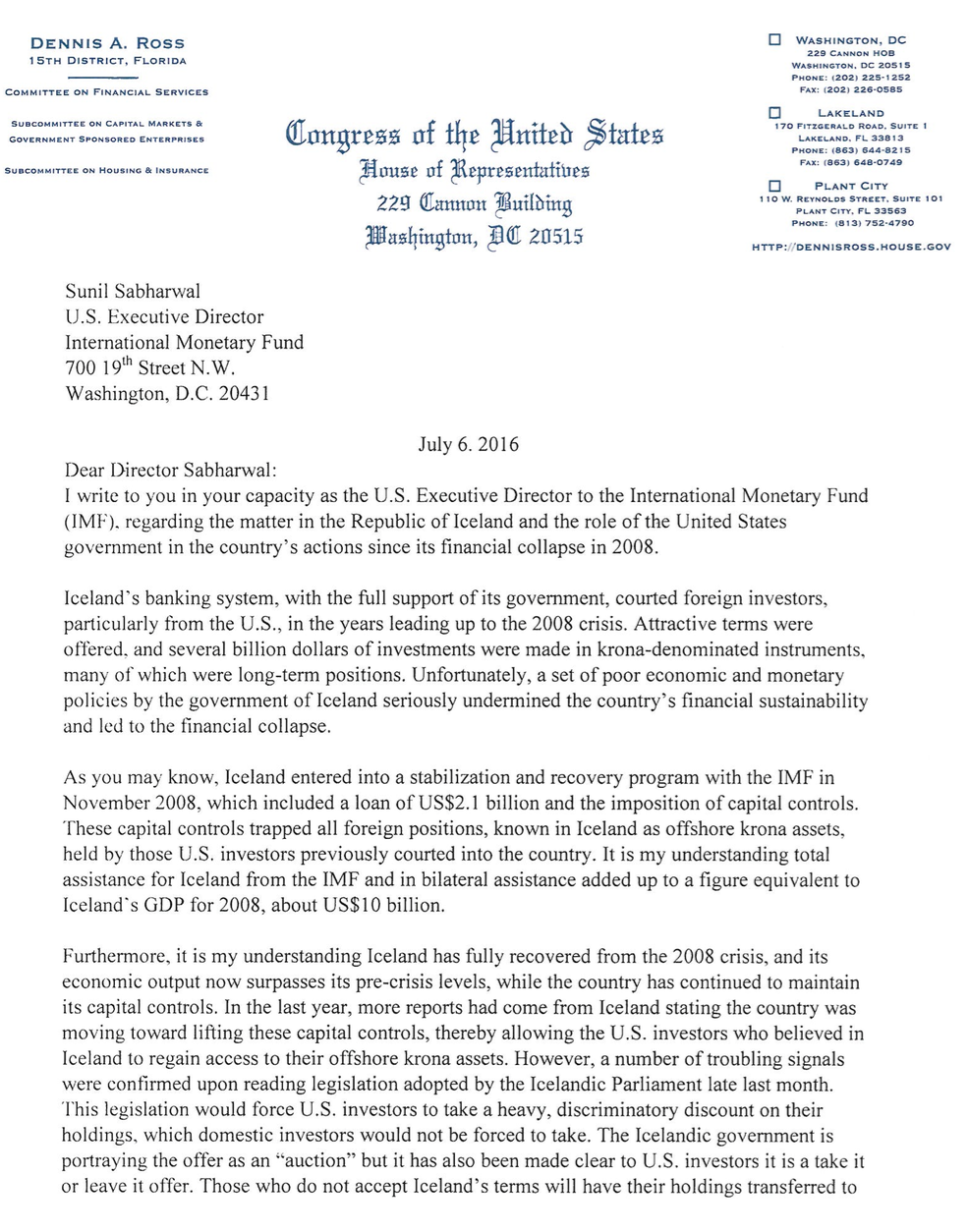

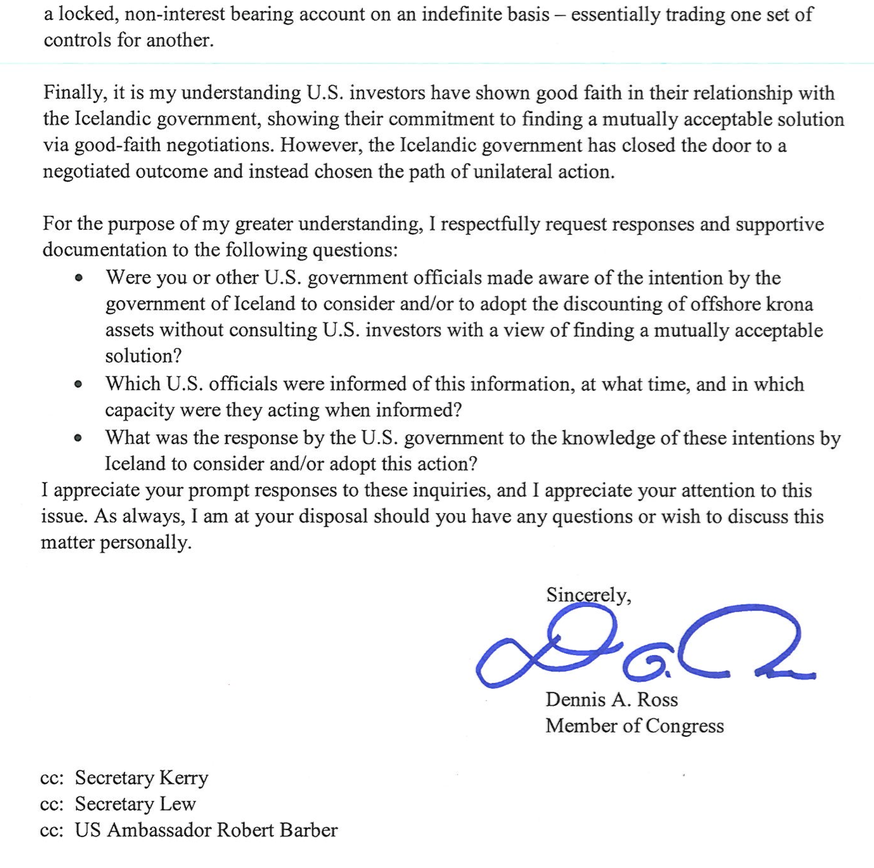

Next step by offshore króna holders: call the IMF

Congressman Dennis A Ross has written a letter, see below, to Sunil Sabharval, US Executive Director at the International Monetary Fund, IMF, inquiring as to what US officials knew about the offshore króna actions taken by the Icelandic government. The Congressman’s mission is clearly to safeguard US interests, i.e. the interest of US funds holding offshore króna, a problem I have dealt with extensively in earlier blogs, inter alia here. Although not stated explicitly, the most sensitive underlying assets are sovereign securities, payable in Icelandic króna.

In the letter the reasons for the Icelandic collapse are somewhat simplified to say the very least, apparently easier to blame the government than the banks; also rather funny to see the offshore króna holders treated as entirely blameless lured by good deals, another saga.

The thrust of the letter is that since Iceland has now recovered well from its 2008 crisis Iceland shouldn’t be discounting the offshore króna or offering the investors punitive terms. – Further to this: intriguingly, Iceland had not made a loss on the 2008 banking crisis but a gain of 9% of GDP(!), according to the latest IMF Article IV Consultation statement on Iceland, from June 22.

The Congressman points out that the offshore króna holders (i.e. the largest holders) have come up with various solution but Icelandic authorities have been unwilling to take any notice. He now wants to know if US officials are aware of what is going on – and he expects an answer, which as far as I know has not yet been given. IMF has preached a cooperative approach to lift capital controls, reiterated in its June statement on Iceland but seems to consent with the action taken by Icelandic authorities re the offshore króna.

Here is Congressman Ross’ letter:

Last time, this time – in general

As I recounted at length in the years, months and days up to the plan to lift capital controls on the estates of the banks, presented June 8 last year, Icelandic authorities dithered for long due to infighting until they took the plunge – to be fair, the authorities claimed it just took time to prepare the plan and refused all allegations of infighting. But the plunge wasn’t taken until it was clear the plan was supported by the largest creditors.

The same now with the offshore króna action, it all took longer than had been planned, my understanding is that it took long because of different views; however, those involved say it just took the time it took, complicated matters etc. Yet, this time the government acted unilaterally, no agreement with the largest offshore króna holders. Thus inter alia the above letter, I assume.

The government claims the offshore króna holders do not act as a group, contrary to the creditors to the old banks. That isn’t wholly correct – each estate had to be dealt with separately and support was sought for each estate. Thus, the creditors were not a unified group but three groups. So much for that argument now re the offshore króna holders.

As a ground for pride Bjarni Benediktsson minister of finance has pointed out that there was no legal aftermath to the plan last year. Quite true but that’s because the plan wasn’t passed until creditors’ support was ensured. Which is exactly the opposite of now where the government has acted unilaterally re the offshore króna holders who consequently have taken the first steps towards legal action.

In addition, there is the concern Congressman Ross shows, as well as articles in the Wall Street Journal and FT Alphaville, as I have mentioned in earlier blogs – offshore króna holders are clearly trying to point out to the world that Iceland, by planning a haircut on the offshore króna assets (when they are converted into foreign currency) doesn’t intend to honour its international commitments.

Last time, this time – in particular

I have earlier pointed out that I was wondering if the Icelandic government was going to make use of some “tricky teleological interpretation” in its dealings with offshore króna holders.

I didn’t explain in any detail what I had in mind but here it is:

Long before the June 8 plan last year, the Icelandic government claimed it couldn’t possibly have anything to do with the composition of three private banks. Right, except that composition was meaningless if it wasn’t clear beforehand how much of the Icelandic assets creditors (only 10% of the assets went to Icelandic creditors, mostly the CBI) could convert into foreign currency. Composition agreement couldn’t be reached until the government had found a solution i.e a haircut, which the creditors could agree to – that was what mostly took so long to solve.

This time, the core of the offshore króna problem is similar regarding sovereign securities. The government can claim that it’s honouring all its obligations as it will pay out any such securities in full and on time… in króna. The thing is that offshore króna holders can – or could, the auction is now over – either choose to convert at ISK190 a euro (the onshore rate is now ISK136, was ISK139 at the time of the auction) or have their króna kept on a special deposit account at 0.5% interest rates with no maturity in sight. The question is if this is seen as fair… or not.

Last year, the government came to the conclusion that it had to step in to facilitate a composition. Now, it’s just shrugging its shoulder and the message is, as I’ve stated earlier, “let them litigate” – alors, last year, the goal was to prevent legal action, this year it’s bring it on…

Follow me on Twitter for running updates.

Getting rid of the offshore ISK: plenty of sticks, carrots uncertain

After markets closed May 20, minister of finance Bjarni Benediktsson introduced a new Bill (text in English) on offshore ISK, now amounting to ISK319bn, around 14% of Icelandic GDP.

As expected, offshore ISK owners are will be offered to participate in an auction. Those who don’t accept the offer will see their funds put into so-called “Central Bank of Iceland certificates of deposit: Debt instruments issued by the Central Bank of Iceland to deposit money banks that hold offshore króna assets in accounts subject to special restrictions.”

The restrictions are special indeed: the debt instrument will only carry interest of 0.5%, to be reviewed every year. In addition, this debt instrument does not have a specified maturity. As interest rates in Iceland are well above 0.5% and not likely to be near this rate any time soon, the offer is to participate in an auction or have the funds locked in at negative interest rates forever and a day, i.e. well below market rates in Iceland.

If the word “expropriation” comes to mind the 4.1 Chapter is on “Provisions of the Constitution and the European Human Rights Convention”:

The recommendations in the bill of legislation have been drafted with the aim of maintaining compliance with the Constitution and the European Human Rights Convention, particularly as regards protection of ownership rights and prohibition of discrimination. Failure to adhere to these principles could create liability for compensatory damages on the basis of Article 72, Paragraph 1 of the Constitution, cf. also the protection of ownership rights according to the European Human Rights Convention, or could constitute illegal discrimination, which would be in violation of the non-discrimination rule contained in Article 65 of the Constitution, cf. also the prohibition of discrimination on the basis of subjective considerations, according to the European Human Rights Convention and the EEA Agreement.

It is clear that the beneficial owners of offshore króna assets are residents and non-residents and that disposal of offshore króna assets has been subject to restrictions ever since the capital controls were imposed. The extraordinary circumstances currently prevailing are considered to justify the transfer of offshore króna assets in the form of electronically registered securities to administrative accounts with the Central Bank of Iceland and the transfer of deposit balances to accounts that will be subject to the special restrictions provided for in the bill of legislation. The same principles lie behind the recommendation that payments due to other offshore króna assets be subjected to comparable restrictions.

It is appropriate to emphasise that the bill of legislation does not represent a transfer of ownership rights. Furthermore, changes in the custody of króna-denominated assets are not conducive to eroding their value, with reference to the fact that the authorisations for disposal will be either unchanged or more liberal. Nevertheless, it can be said that, by stipulating changes in administration of custody, owners’ right of disposal are being restricted as regards the selection of an administrator.

The Central Bank is authorised to charge administrative fees on offshore króna assets, but these fees shall not exceed the Bank’s actual incurred expense. The restrictions in the bill of legislation centre mainly on owners’ right to decide where their assets are held in custody.

The restrictions provided for in the bill are an element in the vital task of reducing the risk attached to the aforementioned offshore króna assets. The conditions prevailing at the time this bill of legislation is presented – i.e., the imposition of capital controls following the financial crisis in autumn 2008, the steps taken since then, and the damage that protracted capital controls do to the domestic economy – are discussed in detail in Section 2. Furthermore, reference is made to the discussion in that section concerning the necessary scope of the measures provided for in the bill of legislation.

The continued restrictions on the right to dispose of offshore króna assets are based on vital public interest considerations. These restrictions are a necessary element of measures to release the pressure that offshore króna assets could put on the exchange rate of the Icelandic króna, other things being equal, and they are also a way to give the owners of the assets the option of releasing them without jeopardising exchange rate stability. The objective of the bill is to enable the liberalisation of capital controls on households and businesses in Iceland, and also on owners of offshore króna assets. (Emphasis mine).

The situation of the Icelandic economy can be debated but it is, for the time being, fairly if not extraordinary good.

The above mentioned “continued restrictions” indicate that as capital controls are lifted on others, those who hold offshore ISK but didn’t want to participate in the auction are effectively kept locked in.

As soon as plan to lift capital controls was announced in June last year, carry trades on the ISK rose. Intriguingly, part of the present locked-in offshore ISK stems from carry trades (actually often long-term investment rather than only hot inflows). This means, that even before the old overhang has been released, new inflows have started – either a sign of the market’s extremely short memory or faith in the Icelandic economy.

The government carefully avoided legal wrangling with creditors of the estates of the fallen banks. The question is if the new Bill does the same trick and leads to a satisfactory outcome for all. The above are points likely to cause consternation among the four largest holders of offshore ISK, all institutional investors. The question is if it’s more important for them to find a solution and finally clarify the situation or if they see the new measures as an infringement on their legal rights.

Follow me on Twitter for running updates.

Lessons on offshore from the Icelandic collapse

After my talk on “Iceland: the offshorisation of an economy” at the Tax Justice Network Workshop on “Corruption and the Role of Tax Havens” I was invited to blog on the Icelandic offshore lessons. Thanks a million to TJN for the invite, the blog is here.

Follow me on Twitter for running updates.